4.2 Shipbuilders Market Shares

4.2.1 The Historical Perspective

The shipbuilding market, as with any commercial market place, is dynamic. The players all seek to gain and utilise competitive advantage. Some are able to adapt to changes and challenges better than others. These abilities may be physical (e.g. the ability to expand capacity via a state of the art, "greenfield" site) or technical or marketing.

Over time, therefore, the world order will change. In many industries, recent decades have seen a progression of industries become dominant in Asia where once they were staples in Europe and/or North America. Added to this, many feel that Asia is becoming the global economic powerhouse in terms of demand and economic development. An example might be the manufacturing of motor vehicles. For much of the 20th century, this business was dominated by European and North American names. Some of these remain - but the emergence of vehicle production in Japan radically redrew the global output map.

These types of change cannot be by-passed by the shipbuilding industry. Consequently, it is important in the context of the relative market positions of different shipbuilders to establish the long-run trends as well as those in the short term. It helps to provide insight into whether reviewing a period from 1997 onwards is ''atypical" of the longer-term trend.

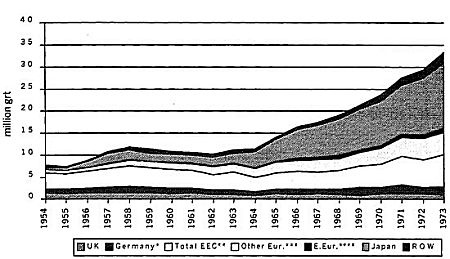

During the 1950s merchant shipbuilding was dominated by Europe. In 1955, Europe built around 4.5 million grt out of the world total of around 5 million grt. The UK contributed 1.3 million grt while (West) Germany was about to reach the 1 million grt level However, the year was also significant in that output exceeded 0.5 million grt in Japan.

By 1965, output had increased to over 11.75 million grt. However, the world order was changing. Japan produced just short of 4.9 million grt (more than the total European output of a decade earlier) while the UK and (West) German figures stood at 1.3 and 1.0 million grt respectively. This was the era of the Japanese "economic miracle". The dramatic rise of a new force in the shipbuilding industry therefore is not new.

Figure 4.7

Historical Completions by Country (grt) - 1954-73

*West Germany **EC-9 ***Finland, Norway, Spain, Sweden, Yugoslavia.

****Poland and East Germany - exc. USSR and other E. European countries Excludes PRC.

Source: Lloyds Register data.

The upheavals in the shipping markets during the early 1970s also led to the widespread introduction of subsidies to support troubled shipyards. This was particularly the case in Europe, where yards were already suffering from Japanese competition.

It is worth considering in order to ascertain whether history provides any pointers to the challenges arising to European shipbuilding in 2000-2001.

By 1972, the OECD accounted for 90% of world shipbuilding output, while Japan and the EEC between them accounted for 73% of total world output. AWES attempts to introduce a degree of output restraint amongst the major shipbuilders were scuppered by disagreements over demand projections between Europe and Japan. SAJ demand projections in 1970 and 1972 were for 32m dwt while AWES projections in 1971 and 1972 were for demand of 25m dwt. By 1974, the tanker delivery schedule was set to peak (in 1975) at around 60m dwt.

Nonetheless, the Japanese were considering restricting their expansion plans due to the rising cost of new berth construction and uncertainties in the Middle East. Meanwhile, European builders were focussing on rationatisation, modernisation and specialisation, with very few new facilities planned. The EC stance was very conservative during this period, with some calls for reserving shares of EEC trade for European built vessels as a reaction to the policy of Japanese shipowners to buy solely from Japanese yards while European owners accounted for some 20% of the Japanese orderbook.

The general view was that the Japanese dominance of the shipbuilding industry was based upon their efficiency, and that links between Japanese yards and financial groups and steel mills was advantageous to the yards. European yards, on the other hand, had few such linkages, and failed to co-operate in terms of pooling steel buying arrangements etc., mainly because of the fragmentation and subsidisation of the European industry.

Table 4.3

Speed of Production: 4 Year Average 1970-73

| Country |

Average number of weeks to finish

(‘000 grt for 1970,1971,1972 & 1973) |

Index

(World Average=100) |

| Japan |

29.23 |

66.3 |

| Denmark |

30.83 |

69.9 |

| West Germany |

52.08 |

118.1 |

| Netherlands |

56.90 |

129.0 |

| Belgium |

58.80 |

133.3 |

| France |

62.40 |

141.5 |

| UK |

74.15 |

168.1 |

| Italy |

116.68 |

264.6 |

| Total EEC |

63.78 |

144.6 |

| Sweden |

40.60 |

92.1 |

| Spain |

67.43 |

152.9 |

| World Total |

44.10 |

100.0 |

Source: Lloyd's Register of Shipping.

During this period, the problems faced by the EEC shipbuilding industry related to outdated plant, well-established foreign competition, reliance on government support, and low profitability. One assessment of "efficiency' was as noted in Table 4.3.

The conclusions of the foregoing assessment points to European shipbuilders losing their first serious market challenge to Japan on the grounds of inefficiency, lack of co-ordination, lack of investment and lack of vision. There was also a subsidy "cushion".

Table 4.4

European Shipbuilding in the Early 1970s:

Strengths, Weaknesses and Missed Opportunities

| Strengths |

Weaknesses |

Missed Opportunities |

| An ability, already proven, to build for the specialised market. |

General disadvantages - national attitudes, labour availability and cost issues, industrial relations systems . |

Despite being responsible for an array of advances in technology, productivity failed to rise. |

| This was identified as LNG carriers, chemical and products carriers, container vessels and Ro/Ro vessels. |

Shipyard groups are far smaller than their Japanese counterparts. |

In part this was attributed to production of devices and tools by a variety of manufacturers in different countries with little or no design co-ordination between them. |

| The short sea market. |

Diverse & fragmented shipbuilding aids & support systems. |

Too many personnel involved in design decisions. |

| "European yards have a fine reputation for product tankers and, as long as they keep abreast shipowners' ideas and changing supply and demand patterns in this sector of the market, the industry ought to retain and increase its proportion of this increasingly important sphere of the market". |

Communication problems between European yards. |

Lack of sufficiently trained personnel to make fully detailed studies of the whole production flow. The Japanese system led to them being in a better position to obtain practical solutions to fundamental problems. |

| Many were seen as "geared" for Handy to Panamax size bulk carriers - and there was hope that the medium sized Japanese yards would move on to larger ships. |

Widely differing codes of practice among shipbuilders, particularly with regard to standards, specifications, etc. |

Inadequate market research into the type and size of vessels that owners require. (In the past, this has rendered expensive equipment obsolete). |

| |

A proportion of output, although decreasing, is dependent upon a mixed product range within existing yards so that a batch-type production rather than a flow line production predominates. (The most successful and efficient yards were identified by (a) high investment, (b) modern management techniques, (c) excellent labour relations and (d) production of standard ships through mass production techniques). |

|

Furthermore, this seems to have marked the turning point, which created what European builders now regard as their "traditional" areas - short sea vessels, plus sophisticated value added vessels.

The conceding of the bulk markets - the relatively unsophisticated bulk carriers and crude tankers - or "market ships" became irreversible. To continue this battle, European builders would have needed to make large-scale investments to pursue what would, more often than not, be low value orders. This process of "catch up" would have been hard to justify logically and financially.

Consequently, increases in capacity and market share gained subsequently by South Korean shipbuilders in pursuit of orders for bulk carriers and crude tankers ought not to be regarded as being issues for European builders. South Korea's emergence threatened Japan. Furthermore, both South Korea and Japan are threatened in this sector by China

4.2.2 Recent Trends in Market Share

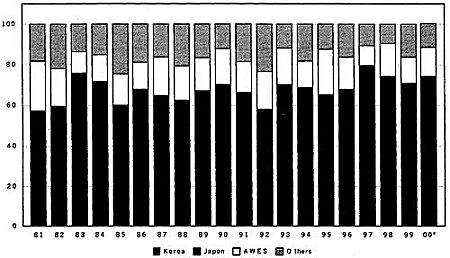

An examination of market shares of new orders (in GT) since the early 1980s shows that the European share of new orders has always been variable. Given that the average AWES market share from 1981 to 2000 has been 16%, with significant swings between individual years (such as 24.5% in 1981 to 10.7% in 1983), the results since 1997 do not actually demonstrate a significant downward trend.

It is apparent that the growth in Korean new orders as a proportion of total new orders in the late 1990s has been at the expense of Japanese yards rather than European yards.

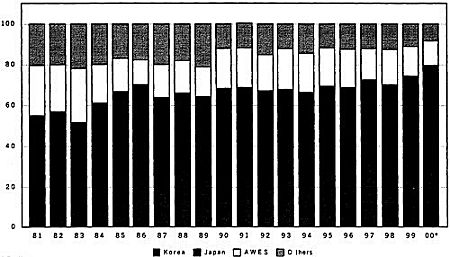

The market share graph for completions shows that although European market shares of completions have fallen slightly in the late 1990s, taking a longer term trend through the 1990s shows European market share has remained fairly steady. In fact, European market share in the 1990s rose from the level of the late 1980s.

Since the shipping market is so cyclical in nature, it is wrong to take a time-scale of only three years, and a longer period beginning in the early 1990s shows a more accurate picture of the market

Korean market share rose significantly in the early 1980s - unsurprising for a relatively new entrant into the market. Thereafter, it held steady until the mid 1990s, after which market share in GT has risen again. This is primarily due to scale economies and productivity improvements, as well as a concentration upon large vessel sizes, which will naturally increase the GT level of completions.

Figure 4.8

Market Share of New Orders by GT

* Preliminary.

NB: Ships over 100 gt. From 1996. Poland is included in AWES.

Source: World Shipbuilding Statistics, Lloyd's

Figure 4.9

Market Share of Completions by GT

*Preliminary.

NB: Ships over 100 gt. From 1996, Poland is included in AWES.

Source: World Shipbuilding Statistics, Lloyd's

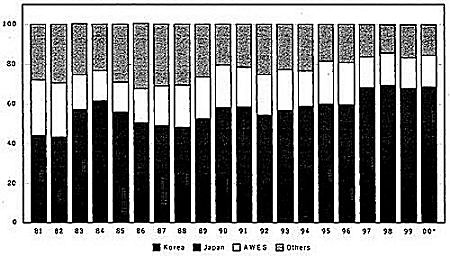

Figure 4.10

Market Share of Orderbook by GT

*Preliminary.

NB : Ships over 100 gt. From 1996, Poland is included in AWES.

Source: World Shipbuilding Statistics. Lloyd's

The Korean share of the orderbook in terms of GT has been growing since the early 1980s. This is not a new phenomenon, and is not surprising given that Korea is a later entrant into the market than both Japan and Europe.

Naturally, Korean yards will initially gain from productivity improvements, economies of scale and learning-by-doing. This is the long-term trend and is to be expected as new entrants to the market improve their technical ability and efficiency.

Older participants in the market are therefore bound to lose some market share, but this does not mean that they will necessarily lose out in absolute terms if total demand also rises.

Again, the figures demonstrate that it is primarily Japan that has lost market share, not Europe.