|

Repairs and Conversions

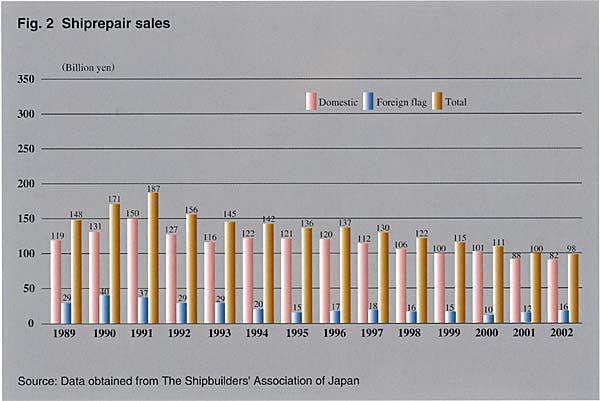

Repair and conversion work in fiscal 2002 earned the industry \98 billion, down 2% from the previous year. The amount of repair and conversion work for fiscal 2002 was the lowest since fiscal 1989. This is due to the fact that the number of domestic and export ships had gradually declined.

Labor Situation

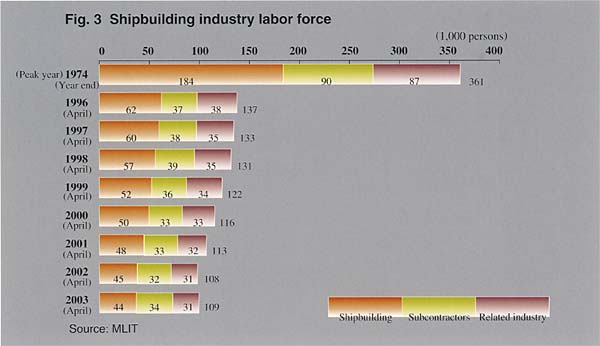

The number of workers engaged in shipbuilding (including those employed by subcontractors) and ship machinery manufacturing was 109,000 in April 2003. The average age of workers at present is over 40 years.

Improved working environment and employment conditions are necessary for facilitating recruitment of young employees, and the industry must also provide training systems to attract a competent staff.

In Japan, shipbuilding facilities are increasingly taking advantage of computer-aided engineering methods such as CAD/CAM in a drive to increase productivity by modernizing and automating the industry and in order to cope with the decreasing and aging population of skilled workers.

The final goal of such modernization is to incorporate CIM (Computer Integrated Manufacturing) using the latest information processing techniques including CALS (Continuous Acquisition and Life-cycle Support) into shipbuilding. Individual shipyards have been conducting R&D on shipbuilding CIM since 1992.

Fig. 2 Shiprepair sales

|

Source: Data obtained from The Shipbuilders' Association of Japan

|

Business situation

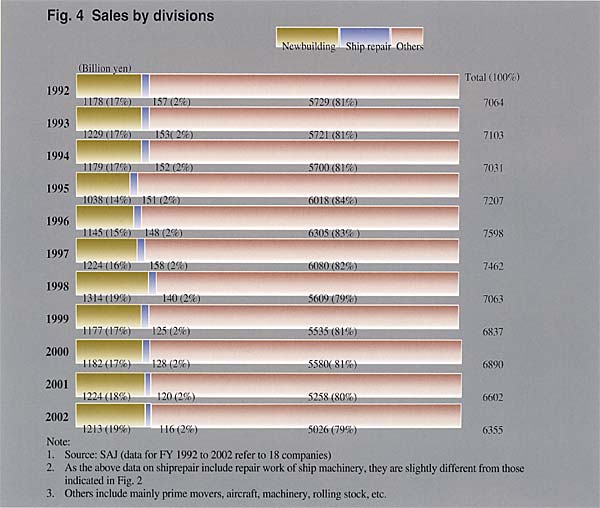

The combined sales of the 18 member companies of the Shipbuilders' Association of Japan were \6,355 billion in fiscal 2002, representing a 4% decrease from the preceding year.

Categorizing total sales by business sector, the shipbuilding business (comprising newbuilding, ship repair and conversion) earned \1,329 billion (down 1.1% from the preceding year) , and all other sectors (heavy machinery, industrial plants, etc.) earned \5,026 billion (down 4.4%).

The share of the shipbuilding sector in total sales was 21% in fiscal 2002. The contribution of the shipbuilding business to the overall sales of the companies averaged 13% for the seven majors and 93% for the 11 medium-size shipbuilders. This indicates a very high proportion of non-marine business in the seven major companies, whereas the 11 medium-size companies are more specialized shipbuilders, relying heavily on the marine business.

Fig. 3 Shipbuilding industry labor force

| Newcastlemax type cape size bulk carrier, NSS Endeavor, built by Mitsui Engineering & Shipbuilding Co., Ltd. |

Challenges

The Japanese shipbuilding industry secured the largest share of the world total of newbuilding orders placed in 2002, and its output in the same year was only slightly less than in 2001. Major and medium-size shipyards are enjoying relatively stable business. However, they are anticipated to be exposed to an even more intense international competition in the coming years, because the supply-demand gap tends to widen and China, in addition to the ROK, is likely to strengthen its production and technical capabilities.

| The first double acting tanker (Ice class 1A), Tempera, built by Sumitomo Heavy Industries Marine & Engineering Co., Ltd. (Sumitomo Heavy Industries, Ltd.) |

Medium-size and major shipyards in such circumstances underwent consolidation or spin-off from the fall of 2002 to 2003, and the structure of the industry changed from the previous setup comprising seven heavy industries companies to two heavy industries plus four dedicated shipbuilders. The industry today is also required to meet such unprecedented problems as the aging of engineers and technicians who have upheld the international competitiveness of Japanese shipbuilders (about half of all the shipbuilding technicians in the country are older than 50 years), increased dependence on subcontractors (the proportion of the work done by subcontracts is 60% or more in major shipyards) and the difficulty in recruiting new graduates of reasonable quality.

Fig. 4 Sales by divisions

|

Source: SAJ (data for FY 1992 to 2002 refer to 18 companies)

|

With a view to formulating a strategy to enable the Japanese shipbuilding industry, which finds itself at a major turning point, to remain competitive in the rest of the 21st century, the Competitive Strategy Conference for the Shipbuilding Industry was set up within the Maritime Bureau of the Ministry of Land, Infrastructure and Transport, and the conference formulated its competitive strategy in June 2003.

Regarding the practical application of new technologies, the first Techno Superliner (TSL) for commercial service is under construction, and is scheduled to begin plying between Tokyo and the Ogasawara Islands in the spring of 2005. The huge floating offshore structure (Mega-Float) has been accepted as one of the candidates for use in the re-expansion of Haneda Airport in Tokyo, and approaches are being made to promote practical use in the construction of airports, disaster relief facilities and public parks.

Smaller shipbuilders mainly supply coasting ships, vessels for short-haul routes and fishing boats, and are suffering a serious depression, as the newbuilding demand for such vessels has plummeted reflecting the large surplus of coasting tonnage, the deterioration of the business of coastal shipping operators and a cutback in the tuna fishing tonnage among other factors. These shipbuilders find themselves in difficult circumstances as newbuilding output and sales have seriously decreased since about 1992. However, the newbuilding demand for smaller vessels is expected to show a basically upward trend in the coming years along with an increase in domestic seaborne trade volume and a progress in the replacement of old tonnage.

|