|

Shipbuilding in Japan

2003

Foreword

Makoto Washizu

Director-General

Maritime Bureau

Ministry of Land, Infrastructure and Transport

The world economy had manifested a stagnant trend due to uncertainties about the future outlook of the economy reflecting, among other factors, the political instability following the September 11 terrorist attacks against the United States in 2001 and the SARS epidemic originating in Asia. However, these uncertainties were clarified by the end of the Iraqi War in April 2003 and the success in bringing the SARS under control, and economic activity has been manifesting a steady upswing, especially in the United States and China.

Against this backdrop of a recovering economic situation in the world, marine transport service has been in tight supply, particularly on account of a marked increase in cargo traffic bound for China, whose economy is enjoying a remarkable boom. This has resulted in very high levels of ocean freight rates, which is also benefiting the shipbuilding industry through an increase in newbuilding orders and a rise in shipbuilding prices.

However, the rise in newbuilding prices does not completely reflect the increase in ordered tonnage, and cost factors are also squeezing shipbuilding business management, such as a rise in steel prices and the strengthening of the yen. As a consequence, shipbuilders are still unable to fully enjoy the benefit of the upswing in newbuilding prices.

Moreover, it is feared that the current high level of shipbuilding demand may be greater than the real requirement, and shipyard expansion plans are being implemented in newly emerging shipbuilding companies. These circumstances may invite a considerable supply-demand gap in the next few years, and drive shipbuilders into an environment of even severer competition.

Given these circumstances, the Japanese shipbuilding industry is making every effort to remain competitive while adapting to the rapidly changing international situation. Major shipbuilders are pursuing greater efficiency in business operations through consolidation or spinning out the shipbuilding division. The Japanese government is also trying to promote further development of the industry by helping create a fair competitive environment in the international shipbuilding market, exploring new demand through the encouragement of R&D work on more environmentally friendly ships, and facilitating the handing-down of craftsmanship from generation to generation in view of the advancing age of skilled workforce.

This brochure describes the current status and the future orientation of shipbuilding in Japan. It is my sincere hope that you will find this publication helpful in deepening your understanding of the Japanese shipbuilding industry.

Japanese Shipbuilding Industry

Current Status

New orders

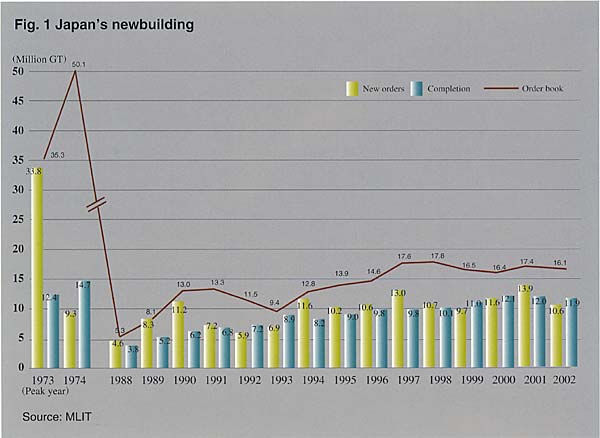

The world total of newly placed shipbuilding orders in 2002 stood at 30,595,000 GT, down 16.2% from the year before, according to the "World Shipbuilding Statistics" of Lloyd's Register. The industry was affected by the stagnation of the shipping market, which had continued until the first half of the year, though the subsequent boom of the shipping market until the year end, coupled with premature replacement orders taking advantage of the prevailing low level of shipbuilding prices, activated the shipbuilding market. Of this global total, Japan accounted for 12,944,000 GT, down 11.0% from 2001 (representing a share of 42.3% on a GT basis), the ROK, for 9,755,000 GT, down 17.6% (31.9%), China, for 3,840,000 GT, down 6.8% (12.6%) and Western Europe (AWES member countries), for 1,621,000 GT, down 56.0% (5.3%).

According to the statistics of construction permits issued by the Japanese government, which cover ships of 2,500 GT and upward (excluding passenger ships), 299 ships of 10,621,000 GT were ordered from Japanese shipbuilders in 2002, down 23.6% in gross tonnage from the preceding year.

To break down the total newly ordered tonnage by the principal type of ship, dry cargo ships totaled 5,770,000 GT (consisting of 162 units) , down 22.2 percent from the year before, and tankers, 6,422,000 GT (136 units), down 24.6%.

Fig. 1 Japan's newbuilding

Among the dry cargo ships, bulk carriers were almost unchanged from 2001 in the number of vessels (123 in 2002 against 122 in 2001) but increased 9.6% in gross tonnage, and the share in the total newly ordered tonnage also rose to 43.9% (against 30.7% in the year before). On the other hand, orders for containerships markedly decreased, totaling only 10 vessels in 2002 against 61 in 2001 (down 81.8% on a gross tonnage basis).

Orders for crude oil tankers totaled 2,588,000 GT, down 40.2% from the year before on a gross tonnage basis, and the share in the total newly ordered tonnage also shrank to 24.4% (against 31.1% in 2001). The 2002 total included nine VLCCs of 1,436,000 GT (against 12 of 1,902,000 GT in the preceding year).

Orders for LPG carriers totaled seven vessels of 155,000 GT (against 23 of 385,000 GT in 2001). On the other hand, orders for chemical carriers and product tankers increased respectively to 42 of 916,000 GT (from 23 of 687,000 GT in 2001) and 51 of 526,000 GT (from 37 of 369,000 GT).

| A 6,492TEU over Panamax, NYK Apollo, built by IHI Marine United Inc. (Ishikawajima-Harima Heavy Industries Co. Ltd.) |

In a classification of the overall newly ordered tonnage into domestic and export vessels, the former totaled 616,000 GT (representing a share of 5.8% in the overall order intake, up 62.5% over the year before), and the latter totaled 10,004,000 GT (94.2% of the total, down 28.0% from 2001).

For supplementary reference, newbuilding orders worldwide in the January-March quarter of 2003 totaled 15,378,000 GT according to the "World Shipbuilding Statistics" of Lloyd's Register, in which the share of Japan was 3,614,000 GT (or 23.5%), that of the ROK, 9,659,000 GT (or 62.8%), that of China, 646,000 GT (or 4.2%), and that of Western Europe (AWES member countries), 599,000 GT (or 3.9%).

Shipbuilding Activities

In fiscal 2002, keels were laid for 359 vessels of 14,034,000 GT (up 14.5% over 2001), 319 vessels of 11,723,000 GT were launched (down 5.3%), and 317 vessels of 11,881,000 GT were completed (up 1.0%).

Order backlog

The combined newbuilding order backlog of Japanese shipyards at the end of June 2003 stood at 384 vessels of 16,097,000 GT, down 7.2% from the end of June 2002. The total comprised 7,900,000 GT of cargo ships and 4,765,000 GT of crude oil tankers.

| An 185,909DWT bulk carrier, Cape Enterprise, built by Kawasaki Shipbuilding Corporation (Kawasaki Heavy Industries, Ltd.) |

| A RO/RO passenger ferry, European Highlander, completed by Mitsubishi Heavy Industries, Ltd. |

|