SECTION 9. IMPACT OF ASIAN CRISIS

The main impact of the Asian crisis upon the Korean shipbuilding industry was felt through exchange movements. The devaluation of the Won meant that, since newbuilding prices are set in US Dollars, Korean yards' incomes in Won increased. Meanwhile, costs remained largely unchanged because the majority of inputs are sourced domestically.

9.1 Exchange Rates

The impact of the Asian crisis in 1997/98 on the global shipping markets was quite pronounced and in shipbuilding it was exchange rate fluctuations that had the most affect.

As far as exchange rates are concerned the main points to note are as follows:

・ Most newbuilding contracts are largely placed in US dollars, with the price being fixed on the contracting date, white many shipbuilding costs, e.g. labour, are normally incurred in domestic currency. In general, around 80% of materials are domestically sourced by Korean shipbuilders, with the remainder being imported.

・ During the Asian financial crisis the exchange rate between the US dollar and the Korean Won changed dramatically, as the poor state of the Korean economy led to a severe weakening in the Won - a fact emphasized by the information in Figure 9.1

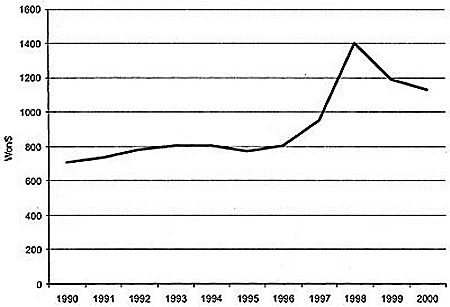

Figure 9.1

South Korean Won vs US Dollar

Source: IMF/Drewry Shipping Consultants Ltd

Figure 9.1 demonstrates that Korean yards gained a huge advantage from the depreciation, from an exchange rate of 800 Korean Won to the US dollar at the end of 1996 to 1,400 Won at the end of 1997. When the Won was at its lowest point in late 1997 Korean yards could have quoted a price over 40% below the prices at which they were quoting in 1996 and still achieve the same Won value as in 1996.

Even today the exchange rate has not recovered to 1996 levels, since the current rate is 1,300 Korean Won to the US dollar, which is therefore still nearly 40% below the exchange rate in 1996.

Without doubt this boosted the competitive position of South Korean yards over all competitors, as they received more Won for all orders placed in dollars. At the same time, domestic costs (labour and materials) were falling due to the weakness in the South Korean economy - hence further improving the competitive position of the yards.

Since the majority of inputs and raw materials used by Korean shipbuilders are sourced domestically, the costs of production were not increased in the way they would have done had imported materials played a significant part in vessel construction. It should be noted that the proportion of inputs sourced domestically is higher for Korean yards than for European yards, therefore European yards are more susceptible to adverse currency movements.

This is not a new phenomenon, as in 1996 the main beneficiary of currency fluctuations was the Japanese shipbuilding industry, which has benefited from a substantial reduction in the value of the yen. At the time this helped to boost the competitive position of Japanese shipbuilders.

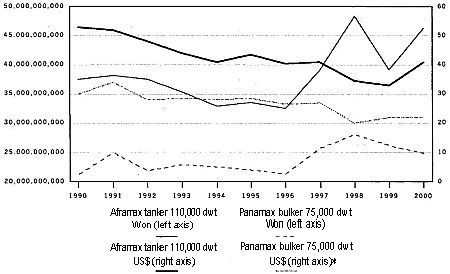

In fact, there have been periods where the Won denominated price of a vessel has actually increased whereas the dollar trend was downward. This was most significantly the case during 1998 at the height of the Asian crisis. Since, as mentioned above, most of the costs faced by Korean yards are in Won, it is this trend which is of greater relevance to the yards when determining what level of newbuilding prices to apply.

Figure 9.2

Newbuilding Prices in Korean Won and US$

* Clarkson data.

Source: Drewry Shipping Consultants Ltd

SECTION 10. NEWBUILDING PRICES

To say that it is only the yards that set newbuilding prices would be to disregard market factors completely. Shipping market cycles, the balance between shipyard capacity and demand, raw material costs, exchange rates and technological developments all play a part in setting newbuilding prices. As such, individual yards do not have sufficient control of the market to dictate prices. Even in sectors where the Koreans have little or no presence, there was a downward trend in newbuilding prices for most of the 1990s.

Newbuilding prices are measured in US Dollars whereas shipyard costs are mainly derived in local currency. Therefore, looking at the Dollar price does not give an accurate picture of the cost position of the individual yards or shipbuilding countries. The role played by exchange rate movements is particularly important given the benefits derived by Korean yards from the devaluation of the Won in the wake of the Asian Crisis.

Also, due to varying yard product mixes and outputs, there are several factors which will create price differences between yards for apparently similar vessels;

・ Reported prices may not be accurate.

・ The vessel may or may not be of a standard design, and the degree of changes from the standard specifications demanded by the customer will vary.

・ It may be a single ship order, or part of a series, or the order may include future options.

・ The vessels may have differing levels of 'bought in' equipment such as engines or containment systems.

・ Existing customers may be offered a more competitive price as some yards place customers relations above the level of profit on each individual contract.

・ Differing financing terms will alter the final cost.

10.1 Newbuilding Price Trends

For much of the last decade newbuilding prices exhibited a long-term declining trend for several reasons:

・ There was excess shipbuilding capacity when new ordering was row.

・ Freight rates were inadequate to justify investment in new tonnage.

・ New shipyard technology brought down the costs of production

・ Prices for inputs for new materials such as steel were falling.

From 1980 to the early 1990s, the pattern, if not the absolute values for newbuilding prices, tends to mirror the health of the shipping markets. Hence, desperate shipbuilders, offering minimum specification ships at ''give away" prices, mirror the very poor freight markets of 1983-86.

In the second half of the 1980s the recovery led to a boom time for shipbuilders, and shipowners generally accepted higher prices as returns from ship operation were more buoyant.

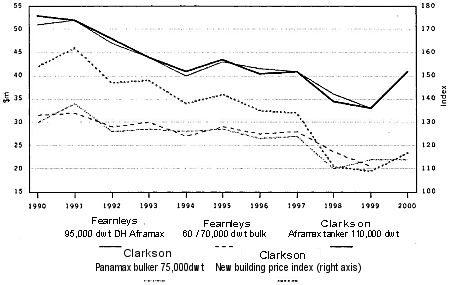

Prices started to collapse in the early 1990s (see Figure 10.1) in response to overcapacity in shipbuilding and reduced new ordering brought about by freight market weakness. The downward trend continued until 1999, in part, because the Asian crisis led to lower wage costs, currency devaluation and falling raw material costs, especially steel.

Since 1999 prices have increased somewhat in response to much firmer freight markets across most sectors, which has resulted in higher levels of new ordering and therefore a tighter balance between shipbuilding capacity and demand.

Figure 10.1

Newbuilding Prices

Source: Drewry Shipping Consultants Ltd

10.2 Factors Affecting Newbuilding Prices

Naturally, prices at any given time reflect the global position of berth supply and demand within the world's shipbuilding yards. As such, no one country has the ability to determine prices in its own right. However, there are other subtle and less subtle variables in determining newbuilding prices.

The main problem with public information is that it is based on reported prices. These may be subject to a margin of error, depending in part on the source they emerge from. However, they seldom (if ever) reveal another vital element - the payment terms. In most business areas, there is likely to be a discount for cash or prompt payment. It may be that, typically, payments are staged (contract signing, keel laying, launching, delivery - with various permutations available). Some deals have payments which are end-loaded, in which case a higher reported price would seem a reasonable expectation. Payment terms may have implications for issues such as refund guarantees. Even for vessels of similar outline specifications, there are valid reasons for price differentials between and within yards.

・ Currency: Although contracts may or may not be costed and quoted in domestic currency, the measure for comparison is the US dollar. Parity rates are shaped by economic prognoses - and can often be driven by sentiment in the market as much as hard reality. Consequently, exchange rates are a vital cog in shipbuilders' success or failure - yet, it is an area in which they have no control.

・ Terms: The phasing of payment structures over the period from ordering to delivery is a variable - early weighting of payments to the yard ought to be a tool to gain some reduction in the benchmark price. Normal terms are likely to see a stream of equal payments normally triggered by a physical development in the process (e.g. deposit, keel laying, delivery, etc.).

・ The size of the order: The ordering of a series of ships ought to gain some price advantage. The owner would expect to see some scale economies passed on white, also, there would be "savings'' in terms of design costs. Adding options to the order may be influential, though much will depend on how the builder rates the probability of the option(s) being exercised.

・ Relationships: A good, longstanding client might reasonably expect some degree of favoured client status. There may also be national trade considerations as well. The nature of existing relationships may also influence issues such as required "guarantees".

・ Ship specialism: At the simplest level, there will be a difference in price quoted between a shipyard's "stock" standard design and either a similar size/type of ''bespoke" design ship, or where the owner requests significant modifications or "add ons" to the "stock" design. However, there are market sectors (examples include open hatch, specially geared bulk carriers or pure car/truck carriers) where price volatility appears surprisingly modest - yet the designs in themselves may be quite consistent, while deals are linked to a small number of established owners.

・ "Political" elements - for example the relationship between Chinese owners and Chinese shipyards; as each has to observe a mix of state dictates and some commercial allowances. Occasionally, yard/vessel owner companies may be interlinked - e.g. Denmark's diverse A. P. Moller (Maersk) group embraces the Odense Steel Shipyard. The Odense yard in Denmark is part of the AP Moller group containing the Maersk and Svitzer shipping companies. The Odense Steer Shipyard group also contains subsidiary yards including Volkswerft Stralsund yard in Germany, Loksa Shipyard in Estonia, Baltija Shipyard in Lithuania and the Odense Marine Services yard at the southern end of the Suez Canal. Since 1995 the Odense main yard at Lindo has delivered 31 vessels(according to Fairplay database of Jan 2001) and has orders for 7 others. Of the 31 vessels, 24 have been built for AP Moller/Maersk and 3 for Svitzer, which is also a subsidiary of the AP Moller group, leaving only 4 for independent customers. AP Moller has also taken delivery of 4 ships from the Volkswerft Stralsund yard in Germany, which is also part of the group.

Absolute price levers are therefore a function of the above, working in conjunction with the wider aspects of shipbuilding capacity, newbuilding demand, raw material prices, currency factors and yard productivity. Newbuilding demand in turn, is a function of the respective health of each shipping market sector, as in a depressed market owners will refrain from ordering new tonnage.

In short to say that the price level is set purely by the yard would be to disregard the role of market forces. For each sector, and indeed in some cases for individual vessel sizes, differing market conditions will dictate different trends in price movements.

10.3 Information - Shipbrokers and How Shipowners Understand the Market

A further factor that might be influential is the supply of information to the customers, and the "quality" of this information. This is crucial to the understanding of ship newbuilding prices. Available information - for many reasons - may be partial and can be "biased". Yet, it is on this information that the shipping industry responds and reacts. Important influences on price knowledge, therefore, are shipbrokers and, in cases where shipowners utilise their services, consultants.

The majority of newbuilding contracts will be arranged through brokers. The owner utilising the broker's services is likely to have ideas on desired specifications and delivery and will be looking for the best price deal based on these. Broker attitudes may well be to target yards, which are "hungry" - e.g. known to have missed out on a previous similar contract. The sellers pay broker's commissions. Consequently, relationships between shipbuilders and brokers can be influential. However, not all brokers will have the same degree of market knowledge and information. Commission, naturally, drives brokers. Ideally, they would like a rising market - and so have the facility to "talk the market up" at times of improving shipping markets. They may also control the access to information.

This is the reason why so much store is placed on the market assessments of major shipbroking houses such as Clarksons, Fearnleys, Platou, SS&Y, etc.

Furthermore, brokers will know which builders are likely to be more flexible in their customer responses. Brokers will not be able to sell what owners do not want, however, they can feedback these requirements, and those yards willing to act on this are likelier to be successful. The flexibility of a yard, in order to meet owners' requirements, is a crucial factor in determining how successful it is in securing contracts.

London is a crucial shipbroking centre. It has the forum of the Baltic Exchange and the head offices of a number of major broking houses - including the world's largest, Clarksons. There are other centres, including Norway, New York, Tokyo and Greece in particular. These are principally owner centres. For this reason, the main Japanese shipbuilders have long established marketing and sates operations based in London and covering "owner contacts" and brokers across Europe. Three Korean builders also have established similar London operations. The marketing stances of European shipbuilders are less obvious.

10.4 Role of Ship Financiers

The vast majority of owners build ships with borrowed money. This can come from a variety of sources but banks/other lenders may impose their own caveats and restrictions. While some transactions may be undertaken via leasing arrangements and, on occasion via ''innovative products" such as bond issues, the main ship finance toot is via the ship mortgage. The position may be different if the shipowner is part of a larger corporate body; they might be treated on corporate client terms. Also, if the project is very costly, the arrangements may embrace funds from a number of banks.

Shipping banks vary from the highly conservative to the highly aggressive. Some have a long-term presence, others are "tourists" who enter in the good time and exit when problems arise. The availability and costs of finance are influential factors in the ability of the owner to place a newbuilding contract. Consequently, commercial ship finance is a factor in the demand equation and so, by implication, must also be a price influence.

Lenders wish to minimise their own risk exposures (as well as make profits). They can, perhaps indirectly, influence ordering choices. Looking at a worst-case scenario foreclosure of the mortgage and ship arrest/repossession - the lender will want an "attractive asset". A well known, successful design has appeal. This can further fuel the shipping industry herd instincts and encourage yards winning orders to secure even more. On the other side of the coin, bank credit committees may limit fending in some geographical areas.