第三部 国際造船市場の変化

-欧州・韓国造船摩擦の背景-

本項では、1990年代における世界の造船市場の変化を振り返り、欧州・韓国造船摩擦の背景について考察した。

3.1 1990年代の造船市場

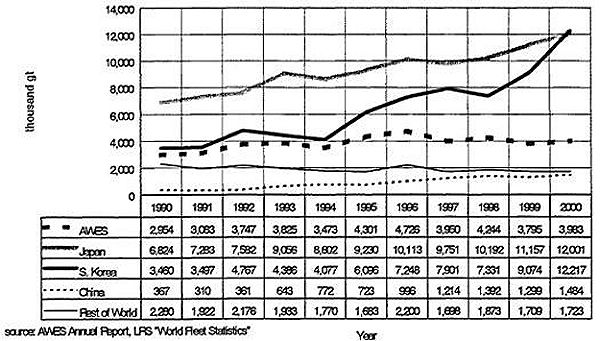

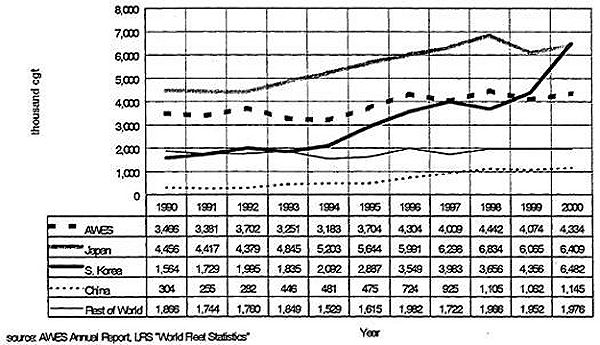

図3.1及び3.2に1990年代の地域別の竣工量の推移をそれぞれ、gt、cgtベースで示した。gtベースでは1990年初頭から既に韓国は欧州を抜き日本に次ぐ造船国となっていたが、90年代終盤にはついにcgtベースでも韓国が欧州を抜き、2000年には僅差ながら日本を抜いて世界最大の造船国となった。

この最大の理由は90年代半ばの韓国における大幅な設備拡張である。本件については、次項で詳述するが、90年代初頭約2百万cgtであった建造量が2000年には6.5百万cgtに達しており、3〜4倍の建造能力の増大を果たしたことになる。大型船の代替建造需要の顕在化や豪華客船の建造ブーム等に支えられ、日本、欧州の建造量も増大したが、日本で2百万cgt、5割増、欧州で百万cgt、3割増と韓国の建造量の増大が圧倒的である。

図3.1 1990〜2000年の世界の地域別竣工量の推移(単位:千gt)

(拡大画面: 60 KB)

図3.2 1990〜2000年の世界の地域別竣工量の推移(単位:千cgt)

(拡大画面: 62 KB)

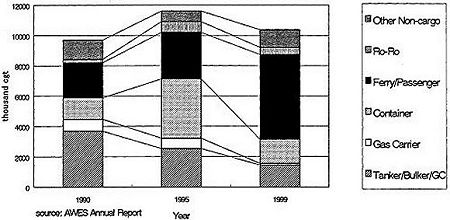

図3.3及び3.4の船種別の手持工事量の変化を見ると、欧州及び韓国の建造船種の変化が如実に把握できる。タンカーやバルカーといった在来型の船種では欧州の建造量は着実に減少し、高付加価値船への転換を指向したコンテナ船やガス船でも90年代後半大きく建造量を失うこととなっている。これを救ったのが90年代後半のクルーズ客船ブームである。欧州は古くから客船を得意としてきたが、このブームでその揺るぎない地位を示し、貨物船市場での敗退を埋める結果となった。ただし、客船の建造能力を有する造船所はノルウェーのクヴァナ、ドイツのマイヤー、フランスのアトランティック、イタリアのフィンカンチエリなど特定の大手造船所に限られており、その他の多くの造船所は特殊船や欧州市場の船種で生き残りをかける状態となっている。

図3.3 欧州の船種別手持工事量の推移(単位:千cgt)

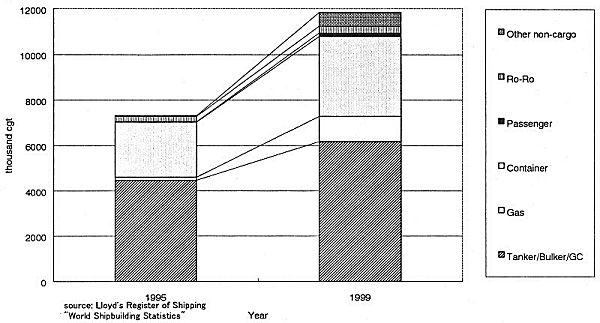

これに対し、韓国は90年代後半で、欧州が市場を失ったタンカーやバルカーといった在来型の船種、ガス船、コンテナ船で大きく手持工事を伸ばしている。

なお、この時期日本はバルカーを中心に在来型の船種で手持工事を増やしたが、欧州同様にガス船、コンテナ船では手持工事の減少を見ている。また、中国は徐々に実力を付けてきたが、量的には大きな影響を及ぼすには至っていない。

図3.4 韓国の船種別手持工事量の推移(単位:千cgt)

(拡大画面: 38 KB)

以上のように、90年代の世界の造船市場の勢力図を総じて見ると、韓国の造船設備拡張により欧州が貨物船市場で大きな後退を強いられ、ニッチな市場でなんとか踏みとどまっているということができよう。造船助成の甲斐もなく、結果的に市場原理により市場から追われた欧州がこれにとって代わった韓国に対し、市場原理に基づく行動を求めるのも理解に難くない。

3.2 1990年代半ばの韓国造船業の設備拡張

韓国は構造調整のため、1988年9月に新造設備の新増設・拡張の凍結、経営合理化、財務構造の改善等を規定した「造船産業合理化法」を施行した。しかしながらこの法律は1993年12月末を期限とする時限法で、市況の回復を見て予定通り廃止された。

こうした中で93年から94年にかけて韓国造船各社から相次いで造船設備の新増設計画が発表された。表3.1に90年代半ばに行われた韓国造船業の建造設備の拡張を示す。

表3.1 1990年代半ばに行われた韓国造船各社の造船設備拡張

| 企業名 |

新設・拡張設備 |

寸法(m) |

備考 |

| 現代重工業 |

建造ドックNo.8(新設) |

360×70×12.7 |

従来の7基の建造ドックに加え、2基を増設 |

| 建造ドックNo.9(新設) |

| 三星重工業 |

建造ドックNo.2(拡張) |

390×65×11.0 |

従来の建造ドック2基中1基を延長し、1基を増設 |

| 建造ドックNo.3(新設) |

640×97.5×12.7 |

| 漢拏重工業 |

建造ドックNo.1(新設) |

500×100×13 |

建造ドックを2基有する造船所を新設 |

| 建造ドックNo.2(新設) |

400×70×13 |

| 韓進重工業(影島) |

建造ドックNo.2(拡張) |

301.5×50×11.5 |

従来の建造ドック3基中1基を延長 |

| 現代尾浦 |

修繕ドックNo.3(転用) |

380×65×12.5 |

従来の修繕用ドック4基中2基を転用 |

| 修繕ドックNo.4(転用) |

300×76×12.5 |

| 大東造船(鎮海) |

建造ドツクNo.1(新設) |

320×74×11 |

建造ドック1基を有する造船所を新設 |

注:韓国造船工業会「造船資料集(97年版)」から作成

国際的協調の下での各国の構造調整により需給不均衡が解消し、やっと市況が回復を始めた矢先であり、韓国造船業の建造能力拡張計画は、需給不均衡を再び招致し、従来の各国の努力を無に帰すものと、欧州、日本の厳しい非難を集めることとなった。

韓国に対する説得の試みは官民両レベルで行われた。1994年3月に開催された第86回OECD造船部会では、欧州、日本に加えて米国も韓国の造船設備拡張について、厳しい批判を行った。各国の主張のポイントは以下のとおりであった。

□ 将来の建造需要、生産性向上による現存設備による建造量の増大を考慮すれば現存設備で十分であり、韓国の設備拡張は過剰建造能力を再びもたらし、船価及び正常な競争に悪影響をもたらす。

□ 構造調整・市場の安定に関する政策協調の指針を定めた「造船政策に関する改訂一般指導原則」に反するものであり、市場において正当化されえないものである。

□ 韓国政府は、造船業への関与に関する造船政策を再考すべき。

□ 各国の懸念を業界に伝えるとともに、建造設備拡張への支援をしないこと、設備拡張により将来困難な事態に陥っても救済を行わないことを明示すべき。

これに対し、造船部会の議事録によれば、韓国政府は、「各国の懸念は理解するも、政府の規制緩和政策及び民業不介入の方針から、造船業の設備拡張の再考を指導することはできない。建造設備規制の廃止は造船合理化法の期限終了に伴うものであり、意図的なものではない。造船業の投資に関する政府支援は行っていないし、これからも行わない。業界には、将来財政的な問題が生じても政府は救済措置をとらないことも伝達済みである。」と回答している。韓国はこの姿勢を貫き通したため、上記の項目を主たる内容とする声明が、日・欧及び米国からそれぞれなされた。

1994年12月の造船協定への署名会合でも、造船能力に関する議長声明の中で、「造船事業者がとった措置により生じる将来のいかなる困難に対しても締約国政府は救済を行わないこと」が謳われるとともに、EC及び米国は再び声明の中で3月の声明で述べた次項に触れている。これに対し、韓国は造船協定に反する造船設備拡張への助成は行うべきでないし、将来設備拡張により困難な事態に立ち至った場合も造船協定に従うべきと声明で述べるに留まった。

【参考】

DECLARATION BY THE EUROPEAN UNION AND JAPAN (March 17th, 1994)

Following the decision of the Korean government at the end of 1993 to end the prohibition on increases of capacity imposed in 1989 in the context of the "Shipbuilding industry rationalisation program" and given the expansion plans foreseen by a certain number of yards, the European Union and Japan:

1. State their strongest concern on the negative consequences of a renewed "overcapacity" at international level with corresponding effects on the level of prices and on normal conditions of competition; In fact, according to all forecasts and taking account of the growth in competitiveness and productivity improvement anticipated by all shipbuilders, existing world capacity is expected to be fully sufficient to accommodate all future building requirement, both in terms of replacement of the fleet and increase in sea-borne trade.

2. Consider that an increase in capacity of Korean shipbuilders, which would in no way be justified by the reality of the market, would seriously undermine the purpose of the Revised General Guidelines for Government Policies in the Shipbuilding Industry and the shipbuilding agreement currently under negotiation which seeks to ensure a balanced market for shipbuilding by way of a return to normal competitive conditions. Such an increase would be an unfortunate return to what could be seen as an artificial "target oriented" commercial strategy seeking to create the situation of "fait accompli" such as existed in the 1970/80s, at a time of deep crisis, when a majority of producing countries were reducing substantially their capacities, important new capacities were installed in Korea. Such policy is still the major cause of the current world problems in the sector.

3. Recall the principle of "solidarity, fairness and international responsibility" set out in the Revised General Guidelines for Government Policies in the Shipbuilding Industry to which the Korean government subscribed in 1990, on its accession to the Working Party No.6 of the OECD.

4. Request the Korean government to reconsider its decision, the consequences of which might damage the sector as a whole and jeopardize the efforts of the Governments of the WP6 to create the conditions under which an equilibrium in the level of supply and demand in shipbuilding industry can be established.

STATEMENT BY THE UNITED STATES (March 17th,1994)

Noting the Korean government's 1993 decision to remove the constraints on shipbuilding capacity expansion that it imposed in its 1989 rationalisation program for the industry and subsequent indications that a number of Korean shipbuilders plan to take advantage of the new policy to expand capacity, and Noting the general consensus of the Subgroup on Supply and Demand of Council Working Party 6 of the OECD in its March 14, 1994 meeting that the planned expansion is not warranted by existing or projected market conditions, the United States:

1. Joins with the European Union, Japan and other parties in expressing is strong concern about the potential impact of the Korean industry's announced plans on the balance of supply and demand in the shipbuilding sector, given an already existing overcapacity;

2. Expresses its hope that the Government of the Republic of Korea will make clear to its shipbuilding industry

-- its intention to neither contribute to the planned expansion nor extricate the industry from any difficulties that expansion may cause in future, and

-- the deep concern the expansion plans have generated among all Council Working Party Members about the prospect of destabilization of the shipbuilding market.

3. Affirms its intention to carefully review the influence of previous and existing Korean government support measures, including the 1989 rationalisation program for DSHM and KSEC, on the announced plans to increase capacity and to carefully monitor developments to ensure that any expansion is carried out without further government support or involvement.

STATEMENT BY THE CHAIRMAN ON FUTURE CAPACITY DEVELOPMENTS IN THE WORLD COMMERCIAL SHIPBUILDING AND REPAIR INDUSTRY THE CHAIRMAN OF THE WORKING PARTY ON SHIPBUILDING OF THE COUNCIL OF THE ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT(December 21st, 1994)(抜粋)

8. Urges governments of Member countries of the Council Working Party on Shipbuilding to ensure that their shipbuilding industries be aware of the concern over world-wide increases in shipbuilding capacities and the obligation of governments under the Agreement not to extricate companies from any future difficulties caused by actions undertaken by shipbuilders;

STATEMENTS BY KOREA ON FUTURE WORK AND ON CAPACITY(December 21st, 1994)(抜粋)

With regard to the shipbuilding capacity increase, the Korean Delegation:

1. draws the attention of the Council Working Party on Shipbuilding to the fact that the issue of capacity increase should be discussed in light of its impact on the future development of the world shipbuilding industry as well as of other related sectors.

2. Finds it not desirable for the Government to intervene in the investment decisions of private enterprises which are taken on a commercial basis in response to the changing market situations.

3. Stresses the importance of full and effective implementation of the Shipbuilding Agreement for the sound development of the world's shipbuilding industry on the basis of market principles.

4. Invites all delegations to reaffirm their assurance that the Governments will not provide any supportive measure to the capacity increase of the shipbuilders which is in violation of the Agreement, and will abide by the Agreement in the future with regard to any difficulties that such an expansion may cause to them.

また、企業間でも1994年3月に開催された日韓欧造船首脳会議(JEK)で、韓国の造船設備拡張問題が議論されたが、韓国側に計画の再考を促す欧州、日本に対し、韓国側は生産量増大を目的とするものでないこと、設備拡張凍結前からの計画であることなどを理由に議論は平行線をたどった。

今日の造船市場の状況は、当時各国が懸念したとおりとなっている。一時的な旺盛な発注に支えられているものの、記録的な受注量・手持工事量にもかかわらず、船価は低水準にとどまっており、過剰建造能力の影響を世界の造船事業者が被っている。大型船の代替需要の消化後の需要の減退による不況が懸念される状況となっている。

韓国政府の将来困難な状況に立ち至っても企業救済はしないとのコミットメントについてみれば、韓国経済危機ともあいまって、造船所の経営難が現実化し、政府や政府系金融機関による救済策がとられた。韓国側は業種横断的な措置や商業上の条件を理由にこれらの措置を問題ないものと主張している。

生産量の増大を目的とするものでないとの造船業界の当時の説明については、前節で述べたとおり、建造量の3〜4倍増が現実であった。

貨物船市場からの撤退を余儀なくされている欧州からみれば、造船政策として見たときの一貫性のない韓国のこれまでの対応を看過し、座して造船業の衰退を待つわけには行かないというのが今回の欧韓造船摩擦の根源であると考えられる。