2. MARKET ANALYSIS

2.1. Market shares

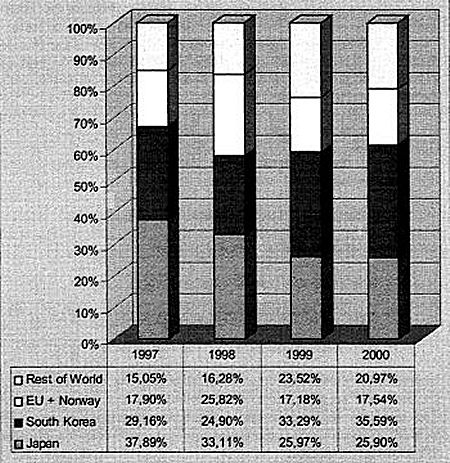

The year 2000 has seen a significant expansion in orders for new ships. Nearly 56 %more orders were placed as compared to 1999, bringing the total volume of new orders to 29,7 Mio. cgt. The larger part of this increase in ordering has been to the benefit of South Korean shipyards which have seen market share increase again. The following graph presents market shares for new order volume based on cgt in the main shipbuilding regions, comparing 2000 with previous years. It should be noted that the data for 2000 is based on available figures which, due to a delay in reporting, are not yet fully consolidated.

Fig.1 - Market shares in new orders in percent and based on cgt, 1997-2000

Source: Lloyd's Register of Shipping

This shows that in 2000, South Korea has consolidated its position as the largest shipbuilding country/region in the world, accounting for more than 35 % of all tonnage ordered world-wide. Therefore the trend described in the previous reports continues. The latest expansion of Korean market share in the period in question has been mainly to the detriment of the "Rest of the World", although affecting different shiptypes (and thus different shipyards) in different ways, while previous expansion of Korean market share had been to the detriment of Japanese and European yards. At the same time South Korean yards face a situation in which ship prices have not recovered from their historical low in 1998/99 and profits are difficult to achieve. To fill the over-capacities in Korea (and recover at least part of the massive investments needed for physical expansion), yards actively seek to generate a high rate of new orders, while at the same time they target higher-value market segments such as gas carriers, containerships or ferries. With all major Korean yards following the same approach, depressed prices now affect all market segments where Korean yards are active. Moreover the fierce internal competition in Korea has led yards to expand capacity even further (e. g, through converting repair facilities into newbuilding facilities as in the case of Hyundai Mipo or lengthening of docks as undertaken by Daewoo), hoping to achieve increased economies of scale and thus a competitive advantage. Consequently, there are no signs that Korean yards will act to stabilise the market and raise prices to commercially viable levels, in particular as yard closures in Korea are politically difficult to implement, and yards continue - as they did in the past - to rely on support from the Government-controlled financial sector when their situation becomes critical.

The fact that, despite the increased Korean market share, the market share for the EU shipbuilding industry (including Norway) has not further deteriorated in 2000 has to be seen in the light of the still booming cruise ship industry. Half(50,1 %) of the cgt volume produced in Europe in 2000 concerns these ships for which there is as yet no Far East competition. Nevertheless, the highly visible efforts of Samsung Heavy Industries to enter the cruise ship market, with some 200 staff assigned to the task, were used by some cruise lines as a leverage to negotiate and obtain lower contract prices with EU yards. While the added value generated by the building of cruise ships may be significant for the EU economy, and the efforts of the EU shipbuilding industry to develop a sound alternative portfolio deserve recognition, it should be kept in mind that only a very limited number of EU yards produce cruise ships. The largest part of the EU shipbuilding yards continues to compete against Far East yards on standard merchant vessels. The situation of some individual yards, in particular those outside the Euro-zone, has become very critical and has resulted in partial closures with significant staff redundancies in 2000 (for example in the UK at Harland & Wolff and at Cammell Laird). Moreover, more and more indications emerge that the current cruise ship boom may soon be over. Over-capacities in the cruise sector already have an impact on prices for cruises, hurting the profits of the cruise companies and making them more reluctant to order new tonnage. The situation of this industry very much depends on economic conditions in the USA(where most of the demand for cruises is located) which now shows signs of weakening. If demand in the cruise sector should falter, this important segment of EU shipbuilding activities will be seriously affected also.

If orders for cruise ships are excluded from the overall figures, the market shares for new orders in 2000 (in cgt) are as follows:

- Korea 39,62 %

- Japan 26,95 %

- EU 9,96 %

- Rest of World 23,47 %.

Another important factor in considering market shares in 2000 is that, in accordance with Council Regulation No 1540/98, operating aid in the EU has been abolished for shipbuilding contracts signed as of 1 January 2001. This deadline has led to a great number of orders placed in EU yards in the last weeks of 2000. Indeed, the overall volume of new orders placed at EU yards in 2000 increased by 64,5 % as compared to 1999, exceeding the overall growth in the world market (56 %). Consequently, and in line with expectations. ordering has been very slow in the first two months of 2001. Only longer term statistics will reveal whether additional orders have been placed or whether, as expected, future demand was simply brought forward. In Japan where domestic demand has always been an important factor, shipyards profited from some new orders from Japanese owners, in particular bulk carriers. Nevertheless, the Japanese shipbuilding industry is currently undergoing a restructuring process with closures of some smaller facilities and mergers between the big shipbuilding groups. The Japanese Government aims to reduce the number of major shipbuilding groups in Japan from seven to three or four. At least two mergers, between Hitachi Zosen and NKK Corp., and between Mitsui Engineering and Shipbuilding, Kawasaki Heavy Industries and Ishikawajima-Harima Heavy Industries, have in the meantime been undertaken or are being concretely discussed, respectively. More restructuring is expected as Japanese yards have been the main victim of aggressive Korean pricing practices, luring away European owners who have traditionally ordered in Japan.

Restructuring efforts also continue in the EU. The two large shipbuilding groups in Spain have been merged, the largest Italian shipbuilder is undergoing privatisation and, in Germany, efforts are being made to consolidate parts of the shipbuilding industry through mergers as well.

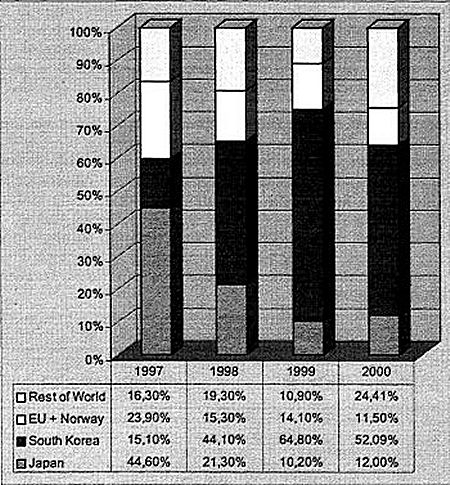

When analysing the market shares for the important segment of containerships, which dominate long-distance liner shipping between the world's main economic centres and which are mainly operated by European shipping lines, the situation is as follows.

Fig. 2 - Market shares in new orders for containerships in percent and based on cgt, 1997-2000

Source: Lloyd's Register of Shipping.

The findings from the previous three shipbuilding reports are confirmed. Korean yards dominate the segment of very large containerships ("Post-Panamax"), leaving only smaller tonnage, for which Korean yards are not well suited due to their size, to EU competitors whose market share in the containership sector has shrunk further. It should be noted that the trend towards much larger ships automatically triggers demand for smaller ships. These smaller ships are needed to supply cargo to the large vessels operating between major hubs. This additional demand has mainly benefited non-EU yards, e.g. in Poland and Croatia, which explains the big market share increase for the "Rest of the World". The commercial volume of these orders is small compared to the volume created by the initial demand for the very large ships. In summary, EU yards lost further market share in the containership segment, while Korea stabilised its leading position, although at a slightly lower level.