|

Japanese Ship Machinery Industry

Production Trends

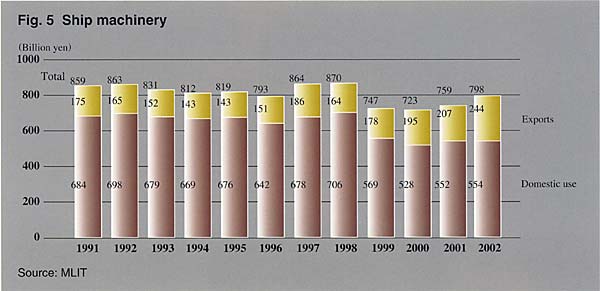

The production trend of the Japanese ship machinery industry is closely related to the newbuilding output of domestic shipyards and the trend of newbuilding prices. The output of ship machinery and equipment in Japan in 2002, though slightly increasing (5.0% over the year before) to \797.5 billion, still remained at a low level, impacted by the stagnation of shipbuilding prices reflecting the intensified international competition for new building orders.

In a breakdown of this total by product category, marine internal combustion engines (marine diesel engines and spark ignition engines) held the greatest share of 38.5% , followed by parts and accessories (for various products of the ship machinery industry including diesel engine parts) constituting 20.0%, outfits (valves, pipe joints, life saving and fire fighting equipment, etc.), 12.6%, and marine auxiliaries (pumps, pneumatic machines, oil treating devices, hydraulic machinery, heat exchangers, electrical machinery including generators, steering gears, etc.), 10.3%.

Fig. 5 Ship machinery

Exports and Imports

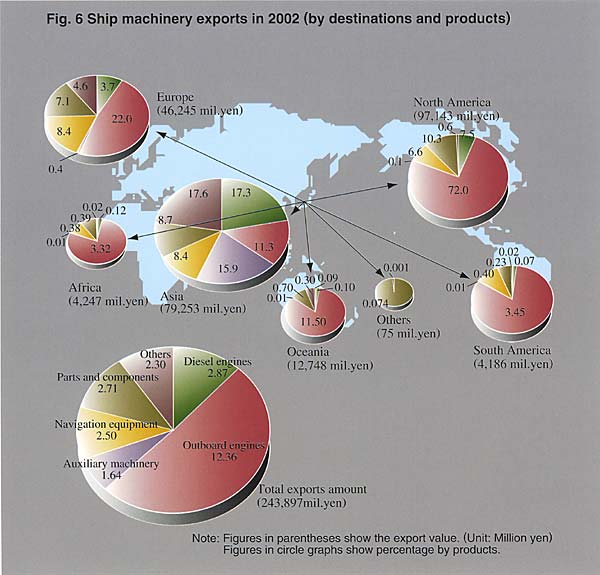

Exports of ship machinery and equipment in 2002 increased 19.6% over the previous year and totaled \243.9 billion. The proportion of exports to the total output value was 30.6%, up 3.7 points. In a breakdown of exports by product category, outboard motors accounted for 50.7% , followed by parts and accessories, 11.1%; marine diesel engines, 10.7% ; navigational equipment, 10.2%; and marine auxiliaries, 6.8% . Classified by geographical destination, 39.8% of the total exports went to North America, 30.3% to Asian countries, and 19.0% to Europe, these three regions absorbing some 90% of total ship machinery and equipment exports from Japan.

On the other hand, ship machinery imports by Japanese shipbuilders and repairers significantly increased, totaling \36.2 billion (up 56.1% over the 2001 total). The shares of major categories were 60.5% for outfits, 14.9% for marine auxiliaries, and 8.7% for marine diesel engines.

Current Status and Challenges

Japan's ship machinery industry consists of 690 factories, and about 31,000 workers are engaged in the industry (as of December 31, 2001).

The industry manufactures a wide variety of products including diesel engines, generators, outfits and navigational instruments, and steadily supplies these items to shipowners and shipyards. The nation is almost 100% self-sufficient in the supply of these products.

Fig. 6 Ship machinery exports in 2002

(by destinations and products)

However, Japanese ship machinery manufacturers now find themselves in a difficult business situation as a consequence of downward pressure on product prices due to the low level of shipbuilding contract prices and stagnation of R&D activities reflecting the protracted recession, in addition to the intensified international competition from European and Asian manufacturers.

In order for Japanese ship machinery manufacturers to remain viable under such adverse circumstances and to continue their steady supply of high quality machinery and equipment to users worldwide, they have to enhance technological development capabilities to adapt to changes in the market, to strengthen financial bases that make such development possible, and to reinforce cost-competitiveness.

Measures Proposed

In view of these needs, the Maritime Bureau of the Ministry of Land, Infrastructure and Transport set up a Subgroup on the Ship Machinery Industry in its Industry Competitive Strategy Conference for the Shipbuilding Industry, which has proposed a strategy for reconstructing the industrial basis and strengthening the international competitiveness of the Japanese ship machinery industry. On the basis of this strategy, the following measures will be taken.

Improvement of Industrial Structure

In order for Japanese ship machinery manufactures to remain strong enough in the competitive environment, which is expected to become even more stringent while adapting themselves to fluctuations in shipbuilding demand, it is essential to eliminate structural destabilizing factors and at the same time to secure an industrial basis and financial strength which would enable adaptation to the business environment. To this end, improvement of the industrial structure will be facilitated by encouraging consolidation, reorganization and alliance, and effective utilization of business resources.

Improvement of Productivity

"Optimization of production processes in the whole shipbuilding industry" and "modernization of the traditional forms of transactions between shipyards and ship machinery suppliers" will be encouraged and, for further enhancement of productivity, the project intended for comprehensive computerized exchange of design and technical information in the ship machinery industry (ZoHaku Web) will be promoted in close cooperation with the shipbuilding industry.

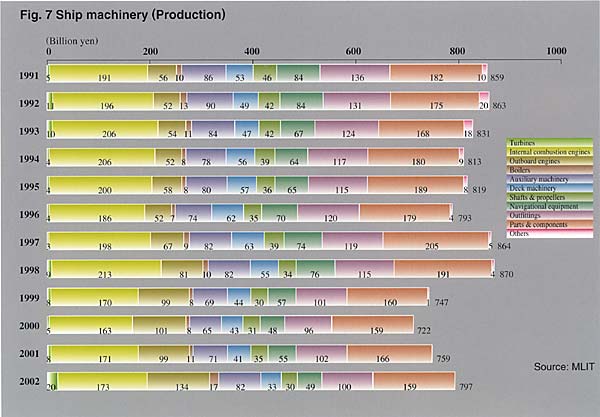

Fig. 7 Ship machinery (Production)

Strengthening of Technological Competitiveness

Today, social requirements regarding ships are becoming ever more diverse and sophisticated as exemplified by the environmental issues ensuing from harmful emissions from ships and the call for increased efficiency of logistics. With a view to precisely identifying these social requirements and user needs, and strengthening the technological capabilities of manufacturers for quickly making available products that can satisfy these needs, technological development to address environmental issues will be given high priority while attempting to "reinforce ties with shipbuilders and shipowners" and to establish "an efficient institutional setup through tightened links between industry, the academic community and the government."

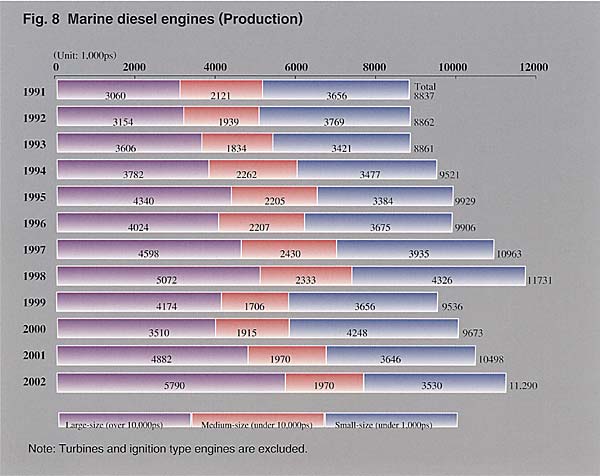

Fig. 8 Marine diesel engines (Production)

|