SECTION 5. PRODUCTIVITY AND COMPETITIVENESS

The primary reason behind the lower newbuilding prices that Korean yards are able to offer is the higher levels of productivity, efficiency and competitiveness enjoyed by Korean shipbuilders.

In terms of labour costs, German labour costs have ranged from being 2.5 to 4 times higher than in Korea. The, already substantial, pre-Asian crisis labour cost advantage enjoyed by Korea was increased even further after the effects of the Asian crisis filtered through. By 1998, Korean labour rates were at least one third of German labour rates.

Korean labour productivity is also significantly higher than European levels. For the period 1996- 1998, Korean labour productivity was 35% higher than German labour productivity, in terms of CGT output per man per year.

When these two factors are combined, the comparison is even more pronounced between Korean yard performance and their European competitors. Overall, Korean productivity adjusted labour costs are around one quarter to one third of German productivity adjusted labour costs. Given that labour costs account for about 20% of the total cost of a Group 1 vessel, the cost saving for a Korean yard is significant.

In short, Korean yards had a substantial productivity advantage over European yards even before the Asian Crisis. Since then, the advantage has increased even further as exchange rate and labour rate factors have come into play

5.1 Competitiveness

The First EU Report on the Situation in World Shipbuilding states that, "It should, however, be recognised that Asian shipyards, in particular in South Korea, are strong competitors in their own right. Yard facilities are often state-of-the-art, the workforce is skilled and flexible and the product quality matches shipowners' demands. Moreover, the local supplier base is able to provide major equipment at significantly lower prices."

In economic terms shipyard competitiveness relates to the cost competitiveness of the whole operation, both in terms of the procurement of materials and equipment and the cost effectiveness of the added value activities that transform these into a finished vessel.

Ultimately it must take into account both the direct costs of ship construction and the recovery of the overhead costs of the operation.

The procurement element is dominated by the direct costs of materials and equipment as the main factor costs of production (other than labour) and, in simple terms, this represents the cost advantage or disadvantage of the shipyard in comparison with other competitor yards. The main issues here would therefore include:

・ Supply markets and price competitiveness of these.

・ Supplier terms including volume discounts.

・ Transport on-costs.

・ Exchange rate effect.

Direct material costs represent a significant proportion of total shipbuilding costs at around 55 - 65% in general terms, and therefore any cost differential can make a significant difference in absolute terms.

In terms of cost effectiveness of the value-added operations that 'convert' procured materials into a completed vessel, the major factors here would include:

・ Labour productivity,

・ Labour cost.

・ Other overhead cost levels and recovery ratios.

Labour costs represent the next major cost element of the shipbuilding process, comprising both direct and indirect labour employed within the yard and the cost of sub-contracted labour services or other temporary labour.

There are two main determinants of labour cost in shipbuilding, namely:

・ Labour productivity

・ Unit costs of labour/employment

Shipbuilding takes place in countries that can have radically different labour cost economies and also productivity levels. However, equal labour cost competitiveness can be achieved in different environments across the spectrum, for example:

・ High productivity combined with high unit labour costs as in Japan.

・ Medium productivity combined with medium unit labour costs.

・ Low productivity combined with low unit labour costs as in China.

At a simplistic level the total labour cost effect can be considered as the mathematical product of the two factors. In general terms, the challenge facing an evolving shipbuilding nation is to retain or improve labour cost competitiveness as its cost environment and manufacturing performance change. To achieve this, productivity must improve at the same rate or faster than labour market costs increase.

Shipbuilding output is generally measured by the 'delivered' CGT within a year, based upon the combined CGT value of all vessels delivered within the year under consideration. CGT is a broad-brush measure of work content and is based upon the Gross Tonnage or Dwt of a vessel (which despite its name is a volume rather than weight measure), adjusted by a compensation factor to reflect the relative complexity of the vessel (hull, machinery and outfit) for different vessel types and sizes.

The compensation factors are developed by an international working party of shipbuilders and updated at regular intervals. CGT, whilst not a precise measure, is the only measure which allows total work content of shipbuilding to be taken into account across a range of vessel types. When used at an aggregate rather than individual vessel level, it is generally accepted to be the best available measure of work content, albeit crude.

The timescale of shipbuilding contracts however is generally long in relation to the yearly cycle used to measure output, and this can therefore lead to significant year-end distortions relating to work-in-progress at the year ends. It is generally accepted in the industry that it is therefore desirable to consider rolling average productivity levels over a period of at least 3 years in order to reduce the impact of such factors and year-on-year activity level variations.

Labour productivity can be monitored in broad-brush terms by the CGT output per person, however, given the varying labour resourcing structures, this needs to include both employees and sub-contract numbers. Where total yard employment is taken into account(i.e. direct and indirect personnel) a gross productivity is determined, reflecting the labour efficiency of supporting operations such as marketing, procurement, business management and administration, as well as production activities.

The simplest measure of unit labour costs is shipyard employment costs, ideally including employment and social on-costs. Clearly different skill levels and staff positions will attract differing remuneration levels, however in view of the dominance of production labour the comparison can pragmatically be made on the level of manual or 'blue collar' employment costs.

Shipbuilding labour cost will generally be incurred domestically and therefore in local currency without exchange rate influences. However, given that most international shipbuilding prices are determined by the US dollar value variations in the exchange rate of the domestic currency against the US dollar, will alter the effective cost of shipbuilding labour between shipyards in different countries.

5.2 Labour Productivity Levels

As a broad brush measure of gross shipbuilding labour productivity, the following CGT/person performance has been calculated using Lloyd's Register statistics for delivered output in CGT and OECD statistics for total shipbuilding manning levels (including subcontractors) on a three year rolling average basis.

The OECD employment figures for the European shipbuilders only include shipbuilding labour, whereas the Korean and Japanese figures also include shiprepair labour. This would unfairly reduce the Japanese and Korean productivity figures since their employment levels would be inflated. Therefore, a factor has been applied for shiprepair labour. The latest available figures for shiprepair turnover as a proportion of total turnover for both Japan and Korea were for 1998 (sourced from the SAJ and KSA).

For Korea, shiprepair accounted for 2.9% of turnover, and for Japan it was 8.4% of turnover. Also, since shiprepair is more labour intensive than shipbuilding, a factor was calculated to account for this. Figures available from AWES provided a breakdown of turnover and employment by shiprepair and shipbuilding. From these, it is possible to calculate the difference in employment levels per unit of turnover for the two activities. Therefore, it is possible to ascertain that approximately 30% more shiprepair labour is required per unit of turnover than for shipbuilding. Combining these two elements meant that the employment figures for Korea and Japan were multiplied by a factor of 0.96 for Korea and 0.89 for Japan in order to get a more accurate comparison with the European figures.

Table 5.1

Average Shipyard Productivity

| Country |

3Year Rolling Average Productivity (CGT/person) |

| 1994-96 |

1995-97 |

1996-98 |

| Germany |

48.1 |

52.8 |

58.8 |

| Italy |

41.6 |

34.1 |

41.9 |

| Poland |

n/a |

n/a |

22.6 |

| Korea |

62.5 |

71.0 |

79.9 |

| Japan |

77.0 |

82.8 |

92.4 |

Notes: 1 Manning levels include sub-contractors

2 Manning levels for Japan & Korea have been factored to compensate for the inclusion of shiprepair activity

Sources: LR Fleet Statistics for CGT output and OECD for manning levels

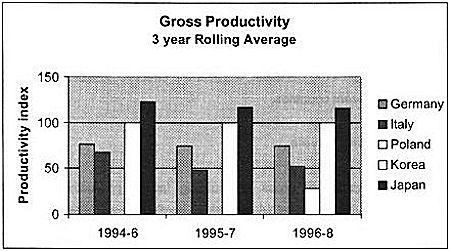

Figure 5.1

Gross Shipyard Productivity

(Korea = 100)

Source: As Table 5.1

Table 5.2.

Indexed Average Shipyard Productivity

(Korea = 100)

| Country |

3Year Rolling Average Productivity (CGT/person) |

| 1994-96 |

1995-97 |

1996-98 |

| Germany |

77 |

74 |

74 |

| Italy |

67 |

48 |

52 |

| Poland |

n/a |

n/a |

28 |

| Korea |

100 |

100 |

100 |

| Japan |

123 |

117 |

116 |

Source: As Table 5.1

These statistics indicate that gross productivity in Korea is significantly higher than in the main EU shipbuilding nations of Germany and Italy, and substantially higher than the relatively newly emerged Polish shipbuilding industry. In relation to Japan, Korean productivity levels are slightly lower, but improving at a higher rate, and therefore closing the gap.

These results are shown in indexed form in Table 5.2 and Figure 5.1 (against Korean performance).

Comparative and reliable productivity information for shipbuilding is hard to achieve but despite the crudeness, omissions and variations of the above data, it is believed that it demonstrates an order of magnitude productivity difference exists between EU and both Japan and Korea.

5.3 Labour Unit Costs

The other key element of overall cost competitiveness is labour costs, which generally reflect the cost economy of the relevant shipbuilding nation as they are incurred in local currency. However, in international terms the effective cost, measured in US dollars per man-year, is influenced by the exchange rate of local currency against the US dollar. This latter factor has had major impact on Korean labour costs since the economic crisis in 1997.

Table 5.3 shows comparative labour costs for the main shipbuilding nations based upon ILO statistics. The costs are presented as annual employment costs to take account of differing employment terms such as annual holiday entitlement and normal working hours per week.

ILO statistics specifically for shipbuilding are not available, therefore, relevant elements from the statistics were extracted. Labour rates for workers involved in related sectors i.e. the manufacture of basic materials, fabricated metal products (except machinery and equipment), machinery and equipment, electrical machinery and other transport equipment were combined to give the average wage for these calculations. Where hourly rates were supplied, they were multiplied by the average working week (as stated by the ILO), monthly rates were multiplied by 12. US Dollar rates were converted using the annual exchange rate figures supplied by AWES.

It can be seen from this information that whilst Korea has experienced a general inflationary movement of labour cost in domestic currency terms, the depreciation of the Won against the dollar has been greater. In particular the impact of the Asian crisis can be seen on the average of daily exchange rates in 1998 and 1999.

Table 5.3

Indicative Labour Costs

| |

Year |

Germany |

Italy |

Poland |

Korea |

Japan |

| Local cost/man-year |

1994 |

103,311 |

|

|

19,125,360 |

|

| Exchange rate vs US $ |

1.6 |

1,613 |

2.3 |

804.3 |

102.2 |

| Cost US $/man-yaer |

63,654 |

|

|

23,779 |

|

| Local cost/man-year |

1995 |

103.502 |

|

|

19,813,440 |

6,239,890 |

| Exchange rate vs US $ |

1.4 |

1,629.0 |

2.4 |

771.4 |

94.1 |

| Cost US $/man-yaer |

72,228 |

|

|

25,685 |

66,311 |

| Local cost/man-year |

1996 |

106,868 |

75,473,120 |

18,079 |

22,064,400 |

6,399,605 |

| Exchange rate vs US $ |

1.5 |

1,543 |

2.7 |

803.0 |

109.0 |

| Cost US $/man-yaer |

71.150 |

48,913 |

6,698 |

27,477 |

58,712 |

| Local cost/man-year |

1997 |

109,344 |

76,730,970 |

22,666 |

24,353,520 |

6,559,320 |

| Exchange rate vs US $ |

1.7 |

1,703 |

3.3 |

950.5 |

121.0 |

| Cost US $/man-yaer |

63,059 |

45,056 |

6,917 |

25,622 |

54,209 |

| Local cost/man-year |

1998 |

111.985 |

77,988,820 |

26,249 |

24,976,680 |

6,719,035 |

| Exchange rate vs US $ |

1.8 |

1,759 |

3.5 |

1400.5 |

130.9 |

| Cost US $/man-yaer |

63,664 |

44,337 |

7,517 |

17,834 |

51,330 |

| Local cost/man-year |

1999 |

114,660 |

79,246,670 |

|

25,599,840 |

6,752,630 |

| Exchange rate vs US $ |

1.8 |

1,822 |

4.0 |

1190.3 |

114.3 |

| Cost US $/man-yaer |

62,931 |

43,494 |

|

21,507 |

59,078 |

Note: 1 Local cost denoted in local currency : Germany - Deutschmark, Italy - Lire, Poland - Zloty, Korea -Won, Japan - Yen

2 Values in italics have been estimated based upon inflation rates

3 Shaded values have been interpolated between other values

Source: Labour costs - ILO labour cost in manufacturing

Exchange rates: AWES - Annual Reports (Average of daily rates)

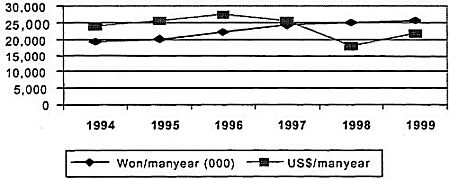

Figure 5.2

Korean Labour Costs

US$ and Won ('000)

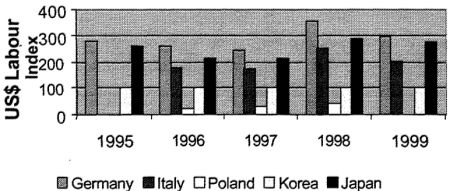

Table 5.4 below shows labour costs in indexed form (against Korea at 100) for the period 1994 - 1999, from which it can be seen that Korea has benefited from a significantly lower labour cost economy than the main Western European shipbuilding nations - Germany, Italy and Japan.

Table 5.4

Indexed Labour Costs

(Korea = 100)

| Country |

Indexed Labour Costs (US $/man-year) |

| 1994 |

1995 |

1996 |

1997 |

1998 |

1999 |

| Germany |

268 |

281 |

259 |

246 |

357 |

293 |

| Italy |

- |

- |

178 |

176 |

249 |

202 |

| Poland |

- |

- |

24 |

27 |

42 |

- |

| Korea |

100 |

100 |

100 |

100 |

100 |

100 |

| Japan |

- |

258 |

214 |

212 |

288 |

275 |

Source: International Labour Office

Figure 5.3.

Unit Labour Costs

Source: International Labour Office

5.4 Korean Labour Competitiveness

It can be seen from the previous sections that the Korean shipbuilding yards enjoy a competitive advantage against the major West European shipbuilding nations in terms of both gross productivity levels and also in terms of unit labour costs.

The combined effect of this is that Korean shipbuilders are in a position to make considerable savings in the labour element of vessel costs, which represents around 20% of total vessel costs. In combining the two index values presented earlier (ie. labour and productivity), an overall labour cost advantage factor of approximately 3 - 4 is calculated for Korea compared with Germany. That is to say that the overall labour element of ship cost in Korea may be approximately 1/3 to 1/4 of Germany.