4.2 RELATIVE POSITION OF KOREA AND EUROPE IN SHIPBUILDING MARKET SECTORS

AWES divides the shipbuilding market into three categories, which for the sake of this Position Paper will be used as a guide to the different sectors:-

GROUP1-tankers and bulk carriers

In this area European shipyards progressively lost market share following the entry of Japanese yards during the 1970's.This trend started before Korean shipyards entered the market, and can not therefore be blamed on Korean shipyards. In response to the challenge from Japanese yards in the tanker and bulk carrier sectors European yards decided to concentrate on more specialised tonnage, and this trend continued after the entry of Korean yards as mainstream competitors in the mid 1980's.

These vessels are the most basic ship type where success is directly linked to efficient volume production of a relatively standardised product. Korean yards have invested in the facilities to build this type of vessel whereas European yards have chosen to concentrate on higher value and more specialised "bespoke" ship types.

The competitive advantage enjoyed by Korean shipyards is most marked for larger tankers and bulk carriers, and European yards have not been able to secure many orders for larger vessels since well before 1997. Accordingly, European yards were no longer very active in this sector of the market prior to the 1997-2000 period covered by the CESA Complaint.

WORLD TANKER ORDER BOOK

1 JANUARY 2001

(Annex 2) |

| SHIPSIZE |

KOREA |

JAPAN |

EU |

CHINA |

POLAND |

OTHERS |

TOTAL |

| 10〜60K DWT |

67 |

16 |

20 |

27 |

10 |

30 |

170 |

| 60〜120K DWT |

48 |

16 |

0 |

7 |

0 |

1 |

72 |

| 120〜200K DWT |

45 |

6 |

0 |

0 |

0 |

7 |

58 |

| 200K + DWT |

58 |

23 |

0 |

5 |

0 |

0 |

86 |

| TOTAL |

218 |

61 |

20 |

39 |

10 |

38 |

386 |

Sources:

1. Newbuilding Order book - Simpson Spence & Young

Note:Norway is classified under EU |

So far as dry cargo bulk carriers are concerned the market leaders are Japanese yards, and it is Japanese yards, not Korean, which have won orders from European yards for this type of vessel. Prices for dry bulk carriers have increased by around 7% in 2000 according to data from Clarksons, but are still depressed. However, since this sector is dominated by Japanese yards this is not the fault of Korean yards. Figures for current orders set out in the table below show that out of a total 517 bulk carriers on order Japan has secured 302 or just under 60%.

WORLD BULKCARRIERS ORDER BOOK

1 JANUARY 2001

(Annex 2) |

| SHIPSIZE |

KOREA |

JAPAN |

EU |

CHINA |

POLAND |

OTHERS |

TOTAL |

| 10〜40 DWT |

12 |

43 |

2 |

35 |

0 |

2 |

94 |

| 40〜60 DWT |

10 |

115 |

0 |

21 |

11 |

21 |

178 |

| 60〜80 DWT |

48 |

100 |

0 |

26 |

0 |

2 |

176 |

| 80 DWT〜 |

18 |

44 |

0 |

0 |

0 |

7 |

69 |

| Total |

88 |

302 |

2 |

82 |

11 |

32 |

517 |

Source:

1. Newbuilding Order book - Simpson Spence & Young

Note:Norway is classified under EU |

In our view the much larger size of Post Panamax container vessel (up to 300 metres in length-similar in size to a VLCC) should in our view be classed as Group1.

Conclusion on Group 1

The decline in orders won by European yards for this type of vessel stared many years ago when European yards lost competitiveness to Japanese yards.

European yards are simply not as competitive for larger tankers and bulk carriers where low labour costs combined with far higher productivity and lower cost of materials give Korean yards a decisive and quite legitimate competitive advantage.

GROUP2 -container vessels, reefers, ro-ro, passenger ferries and multi-purpose vessels.

The position for these types of vessels is more complex since it covers a wide range of vessels. Container vessels are the most important type of vessel within this sector because the order book for reefers, passenger ferries and multi-purpose vessels is very small and not therefore significant.

Containerships

So far as container ships are concerned the market is following the same pattern as for Group 1 vessels, where the ability to build relatively standard vessels efficiently in series gives an advantage to yards which have the facilities and capability to do so at a competitive price. This gives Korean shipyards a natural advantage over European yards, especially for the larger size of Post Panamax container vessel (up to 300 metres in length-similar in size to a VLCC) which should in our view be classed as Group1.

The chart below shows the current order book position as at 1 January 2001.

WORLD CANTAINER ORDER BOOK

1 JANUARY 2001

(Annex) |

| SECTORS |

SHIPSIZE |

KOREA |

JAPAN |

EU |

CHINA |

POLAND |

OTHERS |

TOTAL |

| Small |

100〜499 TEU |

0 |

0 |

0 |

2 |

0 |

3 |

5 |

| 500〜999 TEU |

0 |

4 |

21 |

9 |

1 |

7 |

42 |

| 1,000〜1,999 TEU |

11 |

19 |

16 |

17 |

16 |

14 |

93 |

| Medium |

2,000〜2,999 TEU |

23 |

4 |

25 |

0 |

32 |

15 |

99 |

| 3,000〜3,999 TEU |

9 |

0 |

6 |

0 |

10 |

5 |

30 |

| Large + Post-Pnamax |

4,000〜8,000 TEU |

128 |

24 |

1 |

13 |

10 |

3 |

179 |

| Total |

|

171 |

51 |

69 |

41 |

69 |

47 |

448 |

Source:

1. Newbuilding Order book - Simpson & Young

Note: Norway is classified under EU |

Small: The order book at 1 January 2001 shows that Korean yards did not win any orders for container ships under 1,000 TEU capacity where EU yards won 21.Accordingly there is no basis for the allegation that any injury/adverse trade effect has been caused in this sector.

Korean yards won only 11 orders for ships under 2,000 TEU capacity where prices have remained depressed. German and Polish yards have won most of the orders in this sector (a total of 32) and European yards can therefore hardly complain about unfair competition from Korean yards. In reality, there is substantial price competition between EU yards which must also be taken into account to draw any accurate conclusions on the effects of competition from Korean yards.

Medium: In this sector Korean yards have a slightly smaller number of vessels on order than EU yards, and if orders with Polish yards are included the orders placed with AWES yards then Korean yards have under half the number. Accordingly, EU yards can therefore hardly complain about unfair competition from Korean yards.

Large +Post-Panamax The size of Post Panamax container vessels (up to 300+metres in length-which is similar to a VLCC) means that they belong to a different class from small and medium size vessels.

So far as larger and Post Panamax container vessels in excess of 4,000 TEU are concerned Korean yards have recently been more successful in winning orders than European yards. This is because Korean yards have a natural competitive advantage as a result of their efficiency and resulting ability to build large numbers of relatively standardised vessels involving a substantial weight of steel fabrication at a very competitive cost.

In addition, in order to build the latest generation of larger container vessels above 7,500 TEU it is necessary to have docks of around 340 metres in length which is similar to the size needed to build VLCC's. Korean yards have 12 of these docks available for building such vessels.

A further very important factor is that many container operators want to order a series of 4 or more container vessels for delivery within a short time frame in order to introduce a new container service or upgrade an existing one. This is necessary in order for the operators to remain competitive in the container trades where their rivals are introducing ever larger size vessels to drive down costs. This is confirmed as an important factor in the submissions filed by European shipowners and shipbrokers with the European Commission (hereinafter referred to as the "Third Party Submissions").

Korean yards can guarantee delivery of a series of such vessels within a relatively short time and with reliable delivery dates which European yards can not do, as confirmed by the Third Party Submissions. In addition it is necessary to have the design capability and track record of building larger container ships in order to win orders for the new generation of very large vessels.

LNG carriers

LNG carriers were regarded as being high-tech specialised vessels when they were first introduced in the late 1960's.LNG vessels are now however a well established type of vessel and were first built by Japanese yards in the 1970's.

The standard class of LNG Carrier is currently around 135,000-140,000 CBM. The weight of steel needed to construct such vessels is high at around 33,000 tons, which gives Korean yards a significant competitive advantage over European yards because of the lower cost of Korean steel and their much better productivity as described in the sections below.

In addition, the table below shows that Japanese yards have secured an equal number of orders in this sector. Accordingly, Korean yards are not responsible for European yards failing to win orders in this sector.

WORLD LNG ORDER BOOK

1 JANUARY 2001 |

| SHIPSIZE |

KOREA |

JAPAN |

EU |

CHINA |

POLAND |

OTHERS |

TOTAL |

| 135〜140,000 CBM |

11 |

11 |

3 |

0 |

0 |

0 |

25 |

Source:World Shipyard Monitor -Clarksons

Note: Norway is classified under EU |

Conclusion on Group 2

It is clear that European yards have been successful in winning more orders in the small and medium container ship sector than Korean yards.

European yards are not competitive for the larger new generation vessels. This is however a result of lower productivity, higher labour and material costs and other factors which make them less efficient than Korean yards.

So far as LNG vessels are concerned the high steel weight means that the economics of construction are similar to those for a tanker. This explains why Korean yards have been able to win the same number of orders as Japan because of their superior productivity, lower labour costs and more competitive steel costs.

GROUP3-specialised tonnage.

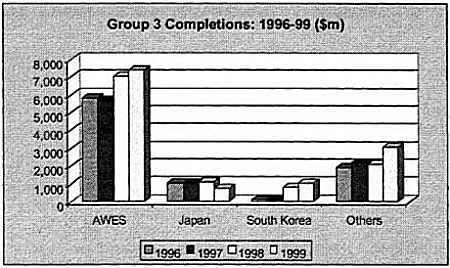

This sector of the market, which includes cruiseships, is dominated by European yards, as can be seen from the bar charts set out below:

Source AWES

The CESA Complaint alleges that Korean shipyards may enter the cruiseship sector, but the evidence is that they have been unsuccessful in attempting to do so.

Korean yards are geared up for volume production, and are therefore unsuited to construction of this type of specialised vessel. As the Commission is aware from their onsite visits earlier this month, the one attempt by a Korean yard to win a cruiseship order at the end of last year was unsuccessful.

Korean yards do not have the industrial base to support cruiseship building, and as a result a large proportion of the materials needed to construct such vessels would need to be imported. This is in contrast with the position so far as Group 1 and Group 2 vessels are concerned where Korean yards can obtain from domestic sources up to 95% of the materials needed for construction. Accordingly, Korean yards do not enjoy the natural advantage possessed by

European yards, or the experience and track record which is essential for success in the cruiseship market.

The reports prepared for the European Commission on the shipbuilding market demonstrate that the largest portion of EU state aid was paid to cruiseships. As this is an area in which the EU yards face almost no competition we question why aid is necessary to support profitability.

GROUP 3 Conclusion

Korean yards do not have a significant market share and there is no clearly foreseeable threat from Korean yards to the European domination of this sector of the market.