付録 1 TBR調査に関するFearnleys社意見書

(2001年3月8日)

WRITTEN OBSERVATIONS

TO THE EU

CONCERNING TRADE PRACTICES ALLEDGELY MAINTAINED

BY SOUTH KOREA AFFECTING TRADE IN COMMERCIAL

VESSELS

PREPARED AND SUBMITTED BY

Fearnleys A/S

Content

| 1 |

PREAMBLE |

2 |

| 2 |

SHIPPING MARKET CONDITIONS 1995-2000 |

2 |

| 3 |

NEWBUILDING ACTIVITY 1990-2000 |

2 |

| 4 |

SUBSIDY SCHERMES |

5 |

| 5 |

COST STRUCTURE OF NEWBUILDINGS |

6 |

| 6 |

CURRENCY RATES OF EXCHNGES |

8 |

| 7 |

CONCLUSION |

10 |

1 PREAMBLE

Upto the late 1960s subsidies, whether direct or indirect, were almost non-existent within the Shipbuilding industry worldwide. In the 1970s, following the sipping market crashes early in that decade, particularly European governments started large-scale subsidy programmes supporting financially troubled shipyards. At this point of time the Japanese shipbuilding industry was at its height and we saw the advent of the South Korean shipbuilding industry.

Aid, or subsidies, to European shipyards increased during the 1980's, whereas during the latest decade we have seen direct subsidy levels being reduced. This does not, however, change the fact that the shipbuilding industry is the most heavily subsidised manufacturing industry within the EU today.

In 2000 CESA, Committee of EU Shipbuilding Associations, lodged a TBR complaint over allegedly unfair competition from South Korean Shipyards.

Allegations of entering loss-contracts, mis-use of IMF funds for industry restructuring, provision of state-aid, etc.

Being concerned by the possible outcome of such TBR, Fearnleys A/S hereby submit our written observations addressing the specific issues raised by the complaint lodged by CESA

2 SHIPPING MARKET CONDITIONS 1995-2000

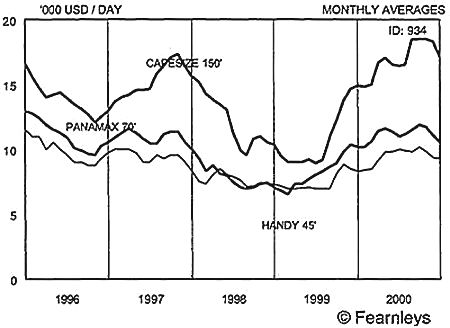

The year 1995 turned to be the best for a long time in the dry bulk market Rates reached heights not seen since the early 1980s. Thereafter, rates declined continuously for a period of almost two years. Towards the end of 1997 rates improved temporarily, however since mid 1997 to autumn 1999 rates declined severely and reached levels that could not cover operational costs, let alone capital costs. Over the past 1 8-month period rates have steadily increased to levels that cover both operational and capital costs of a newbuilding.

DRY BULK 12 M T/C RATES

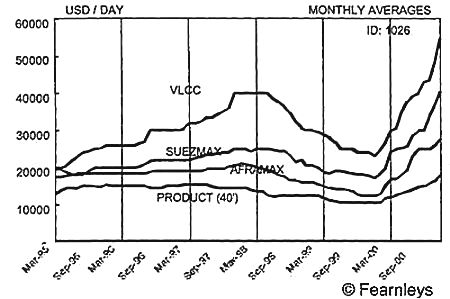

The tanker market fared somewhat differently during this period. Rates increased steadily from 1995 to 1997. However, the levels were not sufficient to cover both operational and capital costs for a newbuild tanker. For a brief period in 1997 rates were at acceptable levels. After this period rates have deteriorated continuously until the spring 2000. Thereafter rates have picked up and reached heights not seen since the boom in the 1970s.

TANKER MARKET 12 M T/C RATES

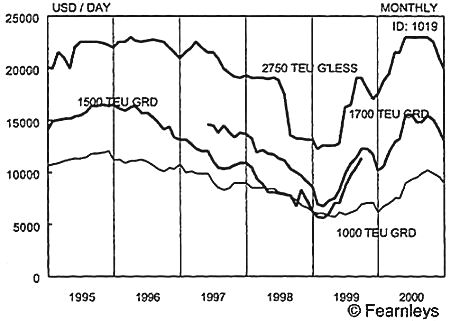

The third major market, container shipping, showed yet again a quite different pattern in rate development. For the three major spot oriented size segments (ships that do not entirely run in the liner operators own programmes but are fixed for shorter/longer term employment in a market with reasonable liquidity) rates were high and defended both operational and capital costs for a newbuilding in the period 1995-mid 1996.

Thereafter rates deteriorated continuously to a level barely covering operational expenses in 1999. Thereafter rates picked up to pre-1996 levels.

CONTAINERSHIP TIMECHARTER RATES

Considering the average earnings over the period 1995-2000 it can be seen that they have been less than acceptable to yield an acceptable return on invested capital for shipowners. The following table gives an overview of average newbuilding prices, average timecharter earnings, and required timecharter rates giving a 10% return on total investment over the lifetime of the ship.

| Shiptype |

Average delivered |

Average tc earnings |

Rquired rate |

| price(Mill USD) |

(USD/Day) |

(USD/Day) |

| Product tanker (45 kdwt) |

31,4 |

13,700 |

15,150 |

| Aframax tanker (105 kdwt) |

40,4 |

18,300 |

18,650 |

| Suezmax tanker (150 kdwt) |

50,5 |

22,400 |

22,950 |

| VLCC (280 kdwt) |

81,1 |

31,100 |

34,250 |

| Handymax bulker (45 kdwt) |

22,9 |

8,800 |

11,450 |

| Pnamax bulker (70 kdwt) |

26,4 |

10,700 |

13,000 |

| Capesize bulker (170kdwt) |

41,0 |

14,900 |

18,350 |

| Cont.ship (1000 TEU) |

22,1 |

9,000 |

9,700 |

| Cont.ship (1500 TEU) |

27,1 |

12,200 |

11,250 |

| Cont.ship (2750 TEU) |

40,1 |

19,700 |

16,800 |

As can be seen from this very brief presentation of the three major shipping segments, only the container shipping market experienced prolonged periods of acceptable returns. Furthermore, it should be noted that all three markets crashed almost simultaneously in 1997. The single most important reason for this crash was the onset of the financial crisis in Asia. With an expanding fleet in all segments, the contraction in seaborne trade led to a significantly poorer climate for shipowners.

Even if there were shorter periods during 1995-2000 yielding acceptable returns to shipowners, we find that on average the market conditions have not been good enough to sustain the prices observed at the beginning of the period. The earnings have not been sufficient to match even average delivered prices. Thus, we believe it is correct to state that during the whole of this period there has been a downward pressure on newbuilding prices.

3 NEWBUILDING ACTIVITY 1990-2000

Considering the shiptypes/sizes targeted by CESA/EU (see table on page 9 of the third report from the Commission to the Council), a total of 2,178 ships delivered during 1990-2000. However, it seems quite clear that the majority of the delivered ships are types no longer being constructed in Europe. Except LNG carriers, containerships and tweendeckers (Multipurpose Ships) European shipyards have not delivered any of the other shiptypes/sizes since 1998. Assuming a normal 18-24 months period from signing of contract to delivery of the ship, EU shipyards have not been able to secure orders for these shiptypes since 1996. Inasmuch as the complaint covers the period from 1997 and onwards, the demise, or lack of competitiveness, was evident long before prices started to tumble in 1997/98. The following table gives an overview of deliveries during 1990-2000:

| |

Total deliveries |

EU deliveries |

Last deliveries |

| Pnamax container carrier |

228 |

98 |

On Order |

| 1,100 Teu Class CC |

552 |

130 |

On Order |

| VLCC |

258 |

13 |

August 1995 |

| Suezmax Tanker |

168 |

35 (incl. 13 Shuttle tankers) |

August 1996 |

| Capesize Bulker |

342 |

6 |

October 1996 |

| Panamax Bulker |

502 |

25 |

November 1999 |

| LNG Carrier |

55 |

11 |

On Order |

| Tween. 15,000 dwt |

73 |

27 |

April 2000 |

| Total |

2,178 |

345 |

|

EU shipbuilders share of world output ranges from 1.8% to 43% over the last decade. However, the large volume segments, it is only within the containership segment where EU shipbuilders have had a large market share. It is furthermore worthwhile to observe that, for the past almost 5 years, EU shipbuilders have not delivered even a single VLCC, Suezmax, or Capesize. According to our sources the same shipyards have not secured an order for such vessels since August 1996.

In our opinion, based on shipbuilding activity the last 5- 10 years, EU shipyards were not able to compete with Asian shipbuilding nations even before 1997.

During the same period world shipbuilding capacity/output has increased significantly.

In 1993 world shipbuilding output was, according to AWES, 12.4 Mill cgt. This figure rose to 17.1 Mill. cgt in 1997 and in 2000 capacity was estimatedly 21.0 Mill. cgt. During this period shipbuilding capacity/output increased in Japan, South Korea, China, and Europe. It is today widely accepted that world shipbuilding capacity is more than ample to meet future requirements for building ships. There is an over-capacity situation in world shipbuilding and this situation has been evident for a number of years. Combined with the financial turmoil, and greatly reduced growth in both GDP and industrial production, in Asia in 1997-99, demand for newbuildings fell and subsequently the overcapacity problems forced shipbuilders to reduce prices.

4 SUBSIDY SCHEMES

In the 1970s, following the shipping market crash, most shipbuilding countries in Europe introduced various forms of both direct and indirect subsidy schemes. They could take the form of direct aid, equity participation, grants, guarantees, soft loans, tax-deferrals and exemptions. Such schemes are still used, however the levels of subsidies are reduced.

In Europe, particularly Germany and Spain have been the countries providing most subsidies to the shipbuilding industry. A few examples:

After the reunification of DDR and BRD it became clear that the former DDR shipbuilding industry was in a poor shape. Several of the Baltic Sea shipyards (Stralsund, MTW, and Warnow) were sold. At the same time the buyers received large direct/indirect contributions for modernising the shipyards and continuing constructing ships. Over a period of 5 years the German Government provided aid in the region of DEM 5 billion for the construction of new docks, fabrication facilities etc.

As a form of indirect aid, the German government provided huge tax exemptions/deferrals for investors in limited partnerships (KG-companies). Although the rules have been changed, this sort of company structure provided much needed capital for ordering containerships in the 1990s. And this system was considered the key incentive for the containership ordering boom at German (and Polish) shipyards in the 1990s. One example:

A 4,500 TEU containership was ordered at a price of USD 65 mill and was delivered in 1997. The delivered price of the ship was DEM 147.7 Mill after finance, fees, commissions, etc. was added. Or, USD 82 Mill. The ship was fixed on a 10-year timecharter at USD 30,700 per day and depreciated to 50% over a period of 12.2 years.

Based on a KG-part of DEM 105,000 and paid-in capital of DEM 39,000, the return on investment (after tax) was a staggering 164.7% of paid in capital. The same project yielded a IRR of 10.67%

Considering the same project as a "conventional" investment, the delivered cost would be USD 68.7 Mill. Based on the same assumptions, the IRR is 12.52%. Considering the total KG investment of USD 82 Mill it is quite interesting to see that the individual KG investor gets such a good return on the investment. Based on a conventional investment analysis of the KG investment (USD 82 Mill.) the required rate would have had to be approx. USD 4.000 per day higher in order to reach the return on the "conventional" investment of USD 68.7 Mill. The difference, as we see it, was picked up by the German government.

As for Spain, we have noted that Spanish shipyards received an "aid package" amounting to ∈1.376 Billion in 1998 alone.

In South Korea we do not know about any direct or indirect forms of subsidies to the shipbuilding industry.

5 COST STRUCTURE OF NEWBUILDINGS

There are several ways to break down the cost structure of a newbuilding. Amongst others, one challenge is to assign indirect costs to a single newbuild. How the individual shipyard spreads its overhead costs. design costs, depreciation of facilities and tools etc on each individual vessel depends on accounting principles, regulatory framework, financing, rate of depreciation, etc. etc. We do not wish to go into details, however it is quite important to highlight some important issues.

In today's' ship newbuilding environment we would in general divide a ship's cost into the following categories:

- Steel material costs

- Main Engine

- Other (e.g. aux systems, electrical, equipment) costs

- Manpower costs

- Other expenses

One could argue that this division is crude and do not give room for "fine-tuning" the cost breakdown. However, for the big cost items we find it sufficient.

Based on studies undertaken at the beginning of the 1990s, the above cost elements' share of the total cost was as follows:

- Steel material costs 23%

- Main Engine 10%

- Other (e.g. aux. systems, electrical, equipment) costs 33%

- Manpower costs 27%

- Other expenses 6%

Each item's relative share maybe changed today but we believe that in principle we have a breakdown in costs similar to the above. South Korea today produces most of the equipment, including main engines, steel and equipment domestically. Engines and other equipment either on licence-built or own designs. Thus, it is not unreasonable to assume that 70-80% of the total cost is based on local, or domestic, sources.

Most modern shipyards, as the South Korean ones, are designed so that, if they were free to choose, they would construct only one shiptype of a certain size, and at a speed that put capacity utilisation just below maximum capacity. The philosophy of the modem shipyard is to construct long series of sisterships that optimises the utilisation of steel fabrication facilities, building berths/docks, etc. By doing so they may spread out design costs. overhead costs etc. and price each ship from the assumed (lowest)cost of the last ship in a series. Furthermore, shipyards are inclined to accept even unprofitable orders securing a high capacity utilisation since reducing utilisation may incur greater losses.

There has been a trend during the last decade that both South Korean and (especially)Japanese shipyards are very little keen on "tailor-made" shiptypes. Even if such projects are profitable, they stir up the production programme for other standard shiptypes and consequently reduce productivity. And as long as the shipyards make their living on standard shiptypes, such tailor- made ships are, generally speaking, unattractive.

European shipyards have been more inclined to entering contracts for speciality ships. In general, with the exception of a few German yards on the Baltic Sea, many of the European shipyards are struggling with old and cramped facilities. Many of them are situated within city limits and have little -or no- room for expansion. Thus the material flow, logistics and facilities for building large blocks are limited and subsequently they have a disadvantage compared with the East Asian shipbuilders. This clearly limits the productivity of European shipyards as well as it makes the basis for further productivity gains within the South Korean shipbuilding industry. As one example, Samsung increased productivity by 15% p.a. in 1996, 1997 and 1998. And by no means was this shipyard poorly managed before this.

Thus, a key element of the South Korean shipyards success is their ability to increase productivity. Even in difficult periods like 1998/99 when prices fell to their lowest since the first half of the 1980s. Additionally, in general the South Korean shipyards have an advantage in modem facilities with ample space to expand into, if necessary.In addition, the modern facilities -combined with effective management systems-secures optimised material flows based on just-time/just-enough principles minimising needs for keeping inventories.

6 CURRENCY RATES OF EXCHANGE EFFECTS

We believe that the single most in1portant factor, leading to the lower prices, is found in exchange rates. In the autumn of 1997, the South Korean Government and Central Bank saw no other solution than to let the WON float. Rapidly, we saw the Won depreciate from a level of WON/USD=880 during the late summer to 1,600 at the end of December that year. This made a tremendous impact on the shipyards earnings.

Unlike their Japanese competitors, South Korean shipbuilders have always accepted contracts in USD. Thus, during the course of a few months, the shipyards almost doubled their income in local currency. Adding to this, interest rates in South Korea soared and it became attractive to enter contracts with front-heavy payments (instead of the standard 5x20% instalments). Without increasing the contractor's delivered cost they could get more money at contract signing, and deposit the excess monies in the financial market with a 20-25% interest.

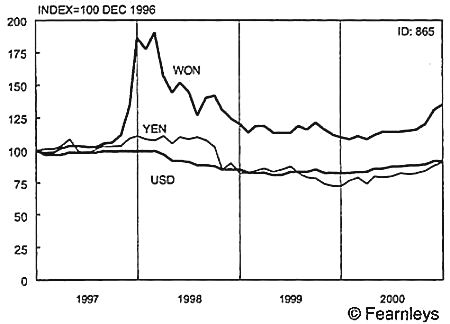

The depreciation of the WON did not affect the cost picture of the shipyards materially. As could be seen in the previous chapter, most of the costs are denominated in local currency. Even though South Korea has to import all rawmaterials for steelmaking, the value added in the steel-making process is in the region of 50% of the steel price. Thus, only half of the 23% steel material costs were affected by the depreciated WON. The following chart shows the contract price for a VLCC newbuilding in WON, Yen, and USD. The timeseries are indexed and based on Dec. 1996-100

NEWBUILDING PRICES VLCC

As the chart clearly illustrates, prices in all three currencies were stable during the first three quarters of 1997. Thereafter, the WON price increased by 80-90% whereas the USD price remained flat. Not until February 1998 did prices start sliding downwards. From mid- 1998 and throughout 1999 WON strengthened towards the USD and this also coincided with USD prices flattening. However, as can be seen from the chart, South Korean shipyards still enjoyed a 25% premium over their end 1996 income even with 15-20% lower USD prices.

In the third report from the Commission to the Council, tables of prices are shown for the purpose Of "proving" that South Korean shipyards in general enter loss-contracts and that prices are lowered below even cost-covering levels. Since these tables show USD prices we find them erroneous and misleading since most of the cost components in Korea are denominated in local currency. Based on the rates of exchange at year-end, and including end of 1996 prices, we have arrived at quite different development in South Korean newbuilding prices.

| USD Prices (Million) |

1996 |

1997 |

1998 |

1999 |

2000/8 |

| Panamax Container Carrier |

52 |

53 |

42 |

38 |

41 |

| 1100 TEU Container Carrier |

21 |

20 |

18 |

17.5 |

18 |

| VLCC |

82 |

83 |

72.5 |

69 |

75.5 |

| Suezmax Tanker |

51 |

52 |

44 |

42.5 |

51 |

| Capesize Bulk Carrier |

39 |

40.5 |

33 |

35 |

39 |

| Panamax Bulk Carrier |

26.5 |

27 |

20 |

22 |

23 |

| LNG Carrier |

220 |

230 |

190 |

165 |

175 |

| Tweendecker 15,000 dwt |

16.5 |

16.5 |

14 |

13 |

13.8 |

| WON/USD Average Dec. rate |

840.9 |

1600 |

1209 |

1140 |

1109 |

| WON Praices (Million) |

1996 |

1997 |

1998 |

1999 |

2000/8 |

| Panamax Container Carrier |

43727 |

84800 |

50778 |

43320 |

45469 |

| 1100 TEU Container Carrier |

17659 |

32000 |

21762 |

19950 |

19962 |

| VLCC |

68954 |

132800 |

87653 |

78660 |

83730 |

| Suezmax Tanker |

42886 |

83200 |

53196 |

48450 |

56559 |

| Capesize Bulk Carrier |

32795 |

64800 |

39897 |

39900 |

43251 |

| Panamax Bulk Carrier |

22284 |

43200 |

24180 |

25080 |

25507 |

| LNG Carrier |

184998 |

368000 |

229710 |

188100 |

194075 |

| Tweendecker 15,000 dwt |

13875 |

26400 |

16926 |

14820 |

15304 |

| Annual Change in WON |

1996/1997 |

1997/1998 |

1998/1999 |

1999/2000 |

1996/2000 |

| Panamax Container Carrier |

93.9% |

-40.1% |

-14.7% |

5.0% |

4.0% |

| 1100 TEU Container Carrier |

81.2% |

-32.0% |

-8.3% |

0.1% |

13.0% |

| VLCC |

92.6% |

-34.0% |

-10.3% |

6.4% |

21.4% |

| Suezmax Tanker |

94.0% |

-36.1% |

-8.9% |

16.7% |

31.9% |

| Capesize Bulk Carrier |

97.6% |

-38.4% |

0.0% |

8.4% |

31.9% |

| Panamax Bulk Carrier |

93.9% |

-44.0% |

3.7% |

1.7% |

14.5% |

| LNG Carrier |

98.9% |

-37.6% |

-18.1% |

3.2% |

4.9% |

| Tweendecker 15,000 dwt |

90.3% |

-35.9% |

-12.4% |

3.3% |

10.3% |

The Commission has, in their report to the Council, based the evolution in prices on end of 1997 figures and denominated in USD. We are of the opinion that firstly, at the end of 1997 there was de facto a financial crisis in South Korea. Secondly, the majority of costs in South Korean shipbuilding are denominated in local currency and at the end of 1997 the WON/USD exchange rate was greatly reduced. Thus, one has to compare with prices observed at a point of time with a "normal" economic Climate and make the analysis in WON.

As can be seen from the table above, prices in August 2000 were on average 16.5%higher than at end of 1996. This can hardly be considered dumping prices and entering contracts well below cost- covering levels.

7 CONCLUSION

Based on our studies we find the allegations and proposed investigations/sanctions of the South Korean shipbuilding industry unjustified. It should also be noted that the allegations are set forth by an industry association with vested interests.

Our opinion is that the reasons for the general fall in USD-prices of newbuildings during the period 1998- 1999 are found in:

- The general market conditions for shipping in this period

- The manufacturing philosophy of modem shipyards

- Excess capacity in world shipbuilding combined with faltering demand

- Increased productivity among South Korean Shipyards

- Change in currency exchange rates favouring South Korean shipyards.

We find the allegations set forth as unjust and wrongful, and urge the EU Commission to stop the process for filing a complaint under the TBR and possibly consequential actions taken by WTO.