5. REFERENCES

Report from the European Commission to the European Council of Ministers on the situation in world shipbuilding, COM (1999) 474 final

Council Regulation (EC) No 1540/98 of29 June 1998 establishing new rules on aid to shipbuilding, Official Journal L 202, 18/07/1998 p. 0001 - 0010

Council Regulation (EC) No 3286/94 of22 December 1994 laying down Community procedures in the field of the common commercial policy in order to ensure the exercise of the Community's rights under international trade rules, in particular those established under the auspices of the World Trade Organization, Official Journal L 349,31/12/1994p. 0071 - 0078

ANNEX: THE SHIPBUILDING INDUSTRY IN THE PEOPLE'S REPUBLIC OF CHINA

The shipbuilding industry in China is diverse but the majority of shipyards are state-owned, primarily within the China State Shipbuilding Corporation (CSSC). State-owned enterprises do not publish detailed accounts and it is questionable whether or not individual shipyards actually know their true costs. Many of the state-owned yards are also heavily diversified and it is difficult to analyse the businesses concerned even from on site.

1999 saw a massive re-structuring of CSSC that came about because the industry is not developing according to expectation. While only a few years ago Chinese yards were seen as a global threat, this threat has largely failed to materialise. he simple fact is that wages and costs have risen considerably in recent years without the necessary performance improvement to ensure competitiveness. The industry is characterised by over-manning and poor performance and the total cost of building a ship in China is regarded by some analysts as being higher than in both Japan and South Korea.

In 1996, CSSC stated that their plan was to double world market share by 2000 from 5% to 10%, achieving an export value of between $1.2 and $1.5 billion. In 1999 the actual share achieved of both gt and cgt was 7%, although it appears that the revenue target may have been accomplished. This is illustrated in the following table using statistics from the Chinese Shipbuilding Industry Association.

Table A. 1 Newbuilding orders in Chinese yards (Source: Lloyd's Register of Shipping)

| |

1997 |

1998 |

1999 |

| Orders from abroad |

2.07 Mio. dwt |

1.712 Mio. dwt |

4.48 Mio. dwt |

| Total orders placed |

2.29 Mio. dwt |

|

8.55 Mio. dwt |

| Total ship export revenue |

1.5 bn USD |

1.73 bn USD |

1.8 bn USD |

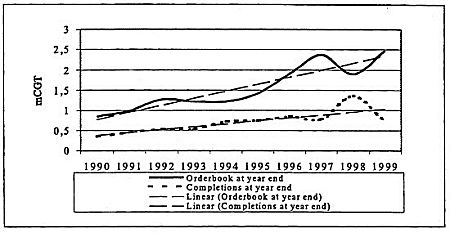

Between the end of 1996 and 1999 the orderbook rose from 1.4 Mio. cgt to 2.5 Mio. cgt, an increase of almost 80%. This is illustrated in the following chart presenting the orderbook since 1990 in terms of cgt and showing the rate of delivery of new tonnage over the same period.

Fig.A.1 - Orderbook and output in Chinese shipyards (Source: Lloyd's Register of Shipping)

Whilst the increase in the orderbook appears impressive it should be seen in context. China has a massive shipbuilding industry (reputedly over 800 shipyards in total, including repair yards) but the orderbook is only marginally ahead of that of Italy (2.1 Mio. cgt) or Germany(2.0 Mio. cgt). It is also an order of magnitude behind the giant orderbooks of South Korea(10.6 Mio. cgt) and Japan (8.6 Mio. cgt). The industry is still many years away from being the global threat that many perceive it to be.

The difference m the rate of increase between the orderbook and deliveries should also be noted from the above graph. Over the period shown, the trend line for increase in the orderbook shows a growth rate of about 17.5% per annum, while for deliveries growth has been about 7.2%. It is concluded from this that the ability to deliver increased tonnage lags the ability to generate increased orders and this is likely to constrain expansion of the industry. It is also likely to lead to production problems with growing backlog and inventory putting increasing pressure on shipyards.

There has been significant capacity expansion in recent years both through the construction of new facilities and the upgrading of existing shipyards. The new facilities are generally finding orders hard to attract due to difficult market conditions and in particular very low prices. A good example is the new VLCC facility at Dalian that has only just managed to attract its first VLCC order, despite trying to get into the market for a number of years. The Chairman of Dalian New Shipyard has lobbied strongly for the devaluation of the Yuan to try to improve competitiveness and help his yard gain orders. These difficulties have not stopped the expansion process, however, including a proposal to build what will be one of the world's largest shipyards at Wai Gao Qiao. There are reportedly five major shipyard projects under construction and a further five in the planning stage.

Investment in new technology has not achieved the gains envisaged. Many shipyards have installed automated panel lines and new construction equipment. The problem is that the shipyards are not yet at a sufficient level of technology to be able to use such sophisticated equipment. Such attempts to buy a way to lower costs are doomed to failure and equipment is not the answer to over-manning and poor management, which are the root causes of low performance in Chinese shipbuilding.

The industry in China is generally characterised by shortage of work and difficulty in attracting new orders. In this respect it should be noted that Chinese shipyards are just as much victims of aggressive Korean capacity as are shipyards in Europe and Japan. Having said this, even without the Korean element it is likely that the yards in China would be short of orders due to inefficiency.

1996 targets for the development of the industry have failed in one further respect of significance to cost investigations. It was stated in that year that by 2000 the use of domestically sourced equipment would account for 80% of equipment used on ships constructed in Chinese shipyards. This has simply not happened, however, with the actual use of Chinese equipment being very limited. Even for vessels built for domestic owners the very poor quality of Chinese equipment means that imported materials are used to a large extent, although import taxes preclude this to some extent.

In summary, the industry in China is in a state of turmoil and actions are being proposed to tackle the problems being faced. The Chinese government has recently announced measures to ensure that ships for domestic operation are built in home shipyards, along with an abolition of taxes and duties previously levied on ships and equipment, to support the industry. However, until the fundamental problems of efficiency are tackled, the industry is unlikely to achieve its true potential.

Restructuring of CSSC

CSSC was founded in 1982 to run the shipyards formerly grouped separately under the 6th Machinery Ministry and the Ministry of Communications (MOC). MOC retained responsibility for a number of smaller yards producing coastal vessels and repairing ships, while CSSC undertook management of the major sectors of the industry.

Although accounts are not published, sources have confirmed that the main thrust behind the restructuring of the state-controlled industry has been huge losses incurred since entering the international market in the early 1980s. The main reasons behind this situation are seen (by the Chinese authorities) to be:

- Poor productivity due to the centralised system;

- Poor management;

- Inefficient planning;

- Lack of knowledge of international practice;

- Corruption.

The support of losses has been the main form of subsidy to the industry in China and the Government has recognised that it needs to adopt truly commercial operations to achieve its aims. To some degree this conflicts with ideology, such as that which precludes the shedding of labour, and there is a long way to go to achieve the aims of the industry. There is also still a long way to go in understanding commercial activity, particularly in state-owned enterprises. For example, it is common practise to hire low cost subcontract labour to work on contracts rather than using more expensive in-house labour, even though the workforce may be under-utilised.

Until the middle of last year, the state-owned industry was primarily, although not solely, under the control of the monolithic CSSC. The industry was basically run by civil servants as a branch of the Government. Following restructuring, the industry will be split into two main groups:

- China State Shipbuilding Corporation (CSSC - southern shipbuilding group, incorporating yards in Guangdong, Jiangxi, Anhui and Shanghai);

- China Shipbuilding Industry Corporation (CSIC - northern shipbuilding group, incorporating yards in Yunnan, Hubei, Tianjin, Shanxi and Liaoning).

These Corporations are ultimately answerable to the Chinese cabinet and will be regulated by the Committee of Science, Technology and National Defence. The larger of the two units is the Bejing based CSIC, having assets of Yuan 9.5 bn (ca. 1.15 bn USD). CSIC holds forty-eight industrial enterprises including Dalian, Dalian New, Qingdao Behei, Liaoning Shipyard and Tianjin Shipbuilding Corporation. This Corporation also operates twenty-eight science, design and research units.

CSSC has assets estimated at Yuan 6.4 bn (Ca. 0.8 bn USD). It operates thirty industrial enterprises including Jiangnan, Hudong, Shanghai, Guangzou Guangdong Shipping and Shanghai Global Container.

The main benefit of restructuring will be the subdivision of the industry into more manageable groups. The main disadvantage is the introduction of competition between the groups and it is not at all clear how this will be resolved. The reforms divide the industry broadly along north/south lines. While the two groups have been given responsibility for managing and increasing asset values for the State, it is left to individual units to determine their product mix and pricing policies. The umbrella groups will not conclude contracts on behalf of the members and will not intervene in day-to-day business unless an activity is deemed to be damaging to the overall industry.

Outside the two main groups there are other commercial shipyards (mainly smaller and local yards) which come under the control of the following organisations:

- Shipbuilders operating under the Ministry of Communications;

- Local shipyards operated by provincial governments in Jiangsu and Fujian;

- Joint venture shipyards (Kawasaki-COSCO, Raffles-Shangdong and Samsung-Ningbo).

In addition, there are a small number of privately owned yards, the main example being Guangzhou Shipyard International. The Government has been reluctant to relinquish control through privatisation and sales and has also been very reluctant to set up joint ventures, having had a number of difficult experiences in this in the past.

There are essentially three main shipbuilding centres in China. Around 50% of shipbuilding output is constructed by yards in the Shanghai region. At the present time, shipyards in Shanghai are limited to building up to about Panamax size due to air-draught restrictions on the Huang Pu river. The alleviation of this restriction is one of the main motivations for the development of the new shipyard at Wai Gao Qiao, outside the restrictions imposed by the river. Dalian is the second most important centre and was chosen as the site of the country's first VLCC yard. Guangzhou is the third important geographical centre and there are other yards located at various sites around the country. The geographical distribution of shipyards is important with regard to costs because costs differ significantly from region to region in China, with Shanghai and Guangzhou being the highest cost locations in the country.

The cost base in Chinese shipbuilding

Labour costs, working practices and performance

China has long been regarded as a low cost country, in particular with respect to wages. This advantage has been eroded in recent years, however, due to increasing wages and standards of living. Inflation has been relentless. Between 1980 and 1998 the annual increase in average wage of staff in manufacturing across the whole country was 16% (source: China Statistical Yearbook) and in absolute terms wages rose by over 400% in the decade between 1988 and 1998.

Wage inflation has not been uniform, however, and variation between regions is very large, with the average earnings in Shanghai being around 90% higher than in Liaoning. There is also a significant variation between different types of company (state-owned or other such as joint ventures, private enterprises and wholly owned foreign enterprises). Of these, organisations with an element of foreign ownership tend to attract the highest payment premiums.

It should further be noted that there is a big difference between rural and urban centres. For example in 1996 average wages in urban centres were almost four times the average in rural areas.

No official productivity statistics have been identified for industry as a whole in China.

However statistics on output per capita for eight major industries are available (source: China Statistical Yearbook), which suggest that productivity has increased over the last decade by only about 3% per annum. In other words, the development of productivity has lagged the increase in the cost base by a significant amount and output prices have therefore risen.

In response to these economic changes and increasing standards of living, in particular in urban centres, costs and prices have risen over the past two decades. The average year-on-year rise in the consumer price index between 1988 and 1998 was 8% (source: China Statistical Yearbook). Again, however, the overall average masks a significant split between rural and urban areas, with the average rise in urban areas over the same period being 10%. In absolute terms consumer prices rose by 2.5 times between 1988 and 1998. Increases have slowed recently due to increased competitive pressure. 1998 saw the first fall in prices on record with a 3% fall in consumer prices in general, although the fall was much less marked in urban areas where a drop of only 1% was seen.

The ex-factory price of industrial goods has also risen in response to the rising cost base. In the ten years between 1988 and 1998 factory gate prices rose by almost 100%, at an average of 9.3% per annum (source: China Statistical Yearbook).

Chinese shipyards tend to be major employers. A typical traditional yard may employ 9000 to 12000 persons. Not all of these workers will be involved directly in shipbuilding, with many yards being diversified, although even given this fact these are huge shipyards in the modern context. Idle time is typically very high (measured recently at around 17% of hours paid in one of the more productive yards) and this, along with inefficiency, means that Chinese yards are in general substantially over-manned. This situation is not helped by the fact that it is not possible under labour law restrictions to lay-off staff as required. The actual rate of over-manning depends on the level of orderbook. If it is assumed that the current relatively high orderbook is associated with an appropriate level of manning, analysis shows that state-owned yards have suffered from levels of over-manning up to double the required number of workers in recent years. The over-manning is further exacerbated by the common use of low cost subcontract labour (typically at about 60% of the cost of using the company's own labour) to take the place of higher cost shipyard workers to reduce the level of direct costs against contracts. This is often done without shedding the labour that is being replaced.

Material costs

China is a major producer of steel and the majority of mild and high tensile steel is sourced locally. Special steels may be imported from Japan or South Korea. Steel prices have been rising steadily within China at an average annual rate of 6% over the last decade. The current price for Grade A steel as used in shipbuilding is probably higher than the price at which steel could be purchased from Korean mills but under the centrally planned system, shipyards are often directed to purchase from local mills, in some cases irrespective of whether the steel is needed or not. This has led to a situation where many of the traditional yards in the state sector are choked with inventory and steel stocks.

Efforts to increase the amount of domestically produced equipment on ships built in China have so far been fruitless. Chinese manufactured equipment, whilst cheap, is not regarded as sufficiently reliable by most shipowners (including Chinese owners) and its inclusion is seen as seriously jeopardising resale values. For this reason the vast majority of equipment is imported. Equipment from Europe and Japan is favoured, with imports from South Korea, with the exception of main engines, being limited. Research is ongoing to evaluate precisely the level of cost advantage enjoyed by Chinese yards. Research to date indicates that domestically sourced equipment is about 30% cheaper than imported, but its use is limited, primarily to basic equipment and equipment built under licence.

Interest rates

The government aims to maintain economic growth at around 8% per annum and is trying to create economic conditions to promote this, including measures to boost consumer spending and infrastructure development. In light of this, and bearing in mind that prices have fallen slightly, the People's Bank of China (PBC) has continuously lowered interest rates in recent years. Rates for working capital loans for state-owned enterprises have declined from about 10% to around 6% since the end of 1996. At January 2000 PBC rates for working capital were 5.85% on a 12-month basis and 5.60% on a 6-month basis. Interest rates for privately owned companies attract a premium of about 30 points, currently standing at about 7.25%.

Exchange rates

Exchange rates have been steady in recent years, almost to the point that the rate between the USD and the Yuan has appeared pegged. There has been a very gradual strengthening in the currency against the dollar, however, which has further reduced competitiveness. Exchange rate movements have, at least in dollar terms, provided little relief from rising costs despite calls from exporting industries (including shipbuilding) to devalue. Loss in competitiveness has been much more marked when the Yuan is measured against the currencies of Japan and South Korea.