Japanese Shipbuilding Industry

Current Status

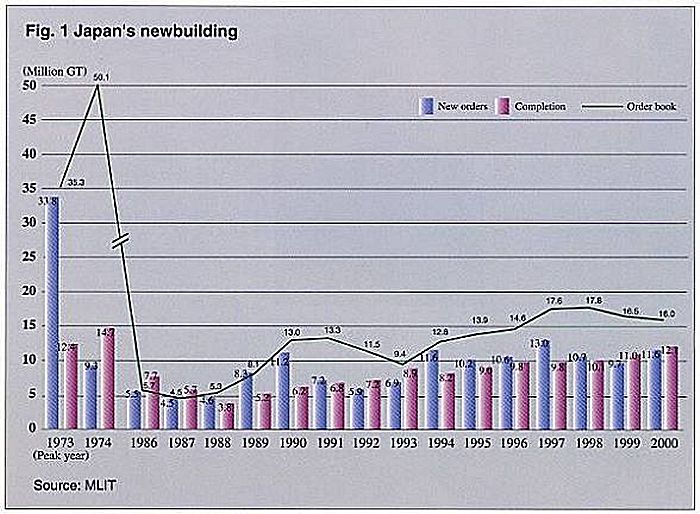

New orders

丂The world total of newbuilding orders in 2000 was the highest since the first oil crisis, as many large oceangoing vessels were due to be replaced and the shipping market was buoyant thanks to the booming U.S. economy among other factors. According to the "World Shipbuilding Statistics" of Lloyd's Register, the global new order intake in 2000 stood at 46,093,000 GT, up 59.2% over the previous year. Of this total, Japan was accountable for 13,475,000 GT, up 54.9% over 1999 (representing a share of 29.2%), Western Europe (AWES member countries), for 6,592,000 GT, up 77.4% (14.3%), and Korea, for 20,791,000 GT, up 75.6% (45.1%).

丂According to statistics on construction permits issued by the Japanese government, which cover vessels of 2500 GT and upward (excluding Passenger vessels), 331 vessels of 11,592,000 GT were ordered from Japanese shipbuilders in 2000, up 19.9% on the number of vessels or 19.6% in gross tonnage over the preceding year.

丂To break down the total tonnage of new orders by the principal type of vessel, dry cargo ships accounted for 8,694,000 GT (against 6,612,000 GT in 1999), tankers, 2,873,000 GT(against 3,032,000 GT), and others, 25,000 GT (against 52,000 GT).

丂

乮奼戝夋柺丗 85 KB乯

丂In a further analysis of dry cargo vessels, bulk carriers increased by 24.1% on a GT basis, and their share in the total tonnage of new orders rose to 59.1%.

丂Orders for crude oil tankers totalled 1,636,000 GT, down 23.9% in GT from the year before, and accounted for 14.1% of the total tonnage of new orders. They included eight VLCCs of 1,270,000 GT (against 11 vessels of 1,741,000 GT in 1999).

丂In 2000, more LPG carriers and LNG carriers were ordered than in the preceding year, respectively totalling 17 of 284,000 GT (against eight of 159,000 GT) and five of 516,000 GT(against one of 109,000 GT). On the other hand, orders for chemical carriers and product tankers decreased respectively to 16 of 176,000 GT (from 23 of 268,000 GT in 1999) and eight of 260,000 GT (from 11 of 345,000 GT).

丂In a classification of the overall tonnage of new orders into domestic and export vessels, while the former totalled 109,000 GT (representing a share of 0.9% in the overall order intake, down 12.1% from the previous year), the latter added up to 11,482,000 GT (99.1% and 20.0%, respectively).

丂For additional reference, newbuilding orders worldwide between January and June of 2001 totalled 21,833,000 GT according to the"World Shipbuilding Statistics"of Lloyd's Register, in which the share of Japan was 8,862,000 GT (or 40.5%), that of Western Europe (AWES member countries), 2,469,000 GT (or 11.3%), and that of Korea, 7,485,000 GT(or 34.2%).

Floating storage and offloading (FSO) facility for oil, Vietsovpetro 01,

completed by Hitachi Zosen Corp.

Shipbuilding Activities

丂In 2000, keels were laid for 288 vessels of 9,930,000 GT (corresponding to 80.2% of the 1999 total), 315 vessels of 11,585,000 GT were launched (102.6% of same), and 323 vessels of 12,112,000 GT were completed (110.2% of same). Thus, while the completed tonnage was greater than the previous year, the keel-laid and launched tonnages were Smaller.

281,395 DWT VLCC, Formosapetro Brilliance, constructed by

Ishikawajima-Harima Heavy Industries Co., Ltd.

Order backlog

丂The newbuilding order backlog of Japanese shipyards at the end of June 2001 stood at 376 vessels of 16,355,000 GT, up 11.9% over the end of June 2000.

丂The total comprised 14 domestic ships of 297,000 GT and 362 export ships of 16,058,000 GT.

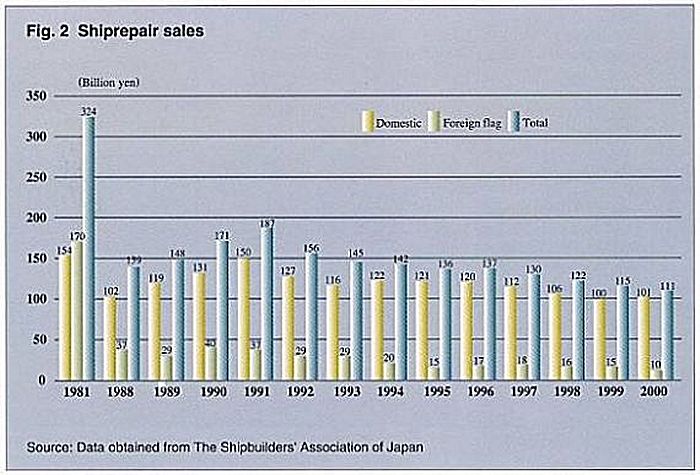

Repairs and Conversions

丂Repair and conversion work in fiscal 2000 recorded a total of \111 billion, down 3.5% over the previous year. The amount of repair and conversion work for fiscal 2000 was the lowest since fiscal 1981. This is due to the fact that the number of domestic and export ships had gradually declined.

丂

84,310m3 LPG carrier, Djanet, constructed by Kawasaki Heavy Industries, Ltd.

Labor Situation

丂The number of workers engaged in shipbuilding(including those employed by subcontractors)and ship machinery manufacturing was 120,000 in April 2001. The average age of workers at present is over 40 years.

丂Improved working environment and employment conditions are necessary for facilitating recruitment of young employees, and the industry must also provide training systems to attract a competent staff.

丂In Japan, further modernization and automation of shipbuilding facilities are now in progress based on computer-aided engineering methods such as CAD/CAM in engineering departments, to cope with the decreased number and aging of skilled workers, while seeking increased productivity.

丂The final goal of such modernization is to incorporate CIM using the most advanced information processing techniques including CALS into shipbuilding. Individual shipyards have been conducting R&D on shipbuilding CIM since 1992.

乮奼戝夋柺丗 71 KB乯

Business situation

丂The combined sales of the 18 member companies of the Shipbuilders' Association of Japan were \6,890 billion in fiscal 2000, representing a 1% increase over the preceding year.

丂In a classification of the total sales by business sector, the shipbuilding business (comprising newbuilding, ship repair and conversion) amounted to \1,310 billion (up 1% over the preceding year), and all other sectors (heavy machinery, industrial plants, etc.) to \5,580 billion(up 1%).

丂The share of the shipbuilding sector in the total sales was 19% in fiscal 2000. The contribution of the shipbuilding business to the overall sales of the companies averaged 12% for the seven majors and 91% for the 11 medium-size shipbuilders. This indicates a very high proportion of non-marine business in the seven major companies, whereas the 11 medium-size companies are more specialized shipbuilders, relying heavily on the marine business.

20,646GT passenger and Ro-Ro ferry, European Causeway, built by

Mitsubishi Heavy Industries, Ltd.