9. IMPACT OF THE ASIAN CRISIS AND DEVALUATION OF THE WON

The CESA Complaint focuses on the period after 1997, which marked the start of the Asian crisis.

All of the newbuilding contracts with which the complaint is concerned are placed in US dollars, with the price being fixed on the date of contracting. Overall up to 80% of the materials and equipment will be sourced in Korea, with only 20% being sourced on the international market.

Accordingly, the dramatic fall in the value of the Won following the Asian crisis provided a dramatic boost to the competitive position of South Korean yards over all of their competitors including in particular Japan and Europe.

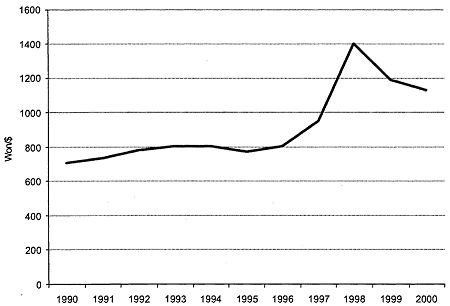

The impact of this can be seen from the graph below, which is based on monthly average exchange rate figures taken from the Financial Times:

It is apparent from this graph that Korean yards gained a huge advantage from the depreciation from an exchange rate of 800 Korean Won to the US dollar at the end of 1996 to 1,750 Won at the end of 1997. When the Won was at its lowest point in late 1997 Korean yards could have quoted a price over 40% below the prices at which they were quoting in 1996 and still received the same value in Won. Yearly average exchange rate figures from the IMF, which are shown in the Drewry Shipbuilding Report, show a lowest average exchange rate of 1,400 Won to the US Dollar during 1997. However, even on the basis of these averaged figures it is clear that Korean yards obtained a huge, and quite legitimate, advantage from the depreciation of the Won.

The exchange rate has not recovered to 1996 levels since the current rate is 1,300 Korean Won to the US dollar. This is still nearly 40% below the exchange rate of 800 Korean Won to the US dollar in 1996.

The CESA complaint focuses entirely on the period between 1997 and 2000, which matches the period following the collapse of the Korean Won against the US Dollar. It is clear against this background that one of the major factors which has allowed Korean yards to quote lower prices since 1997 was not illegal subsidies as alleged by CESA, but the depreciation of the Won against the US Dollar.

CONCLUSION

It is very clear that the depreciation of the Won against the US Dollar in 1997 made Korean yards more competitive and allowed them to quote lower prices than European and Japanese yards.

10. CONCLUSION - EFFECT OF THE COMPLAINT

The CESA allegations are strongly denied. European Yards lost their dominant position in the Shipbuilding market to Japan in the 1960s and 1970s before Korea built up any significant market share.

European Yards had already lost the ability to compete with either Korea or Japan for larger series built vessels such as tankers, bulk carriers and large container vessels well before 1997. Lower labour costs, much higher productivity and lower materials costs give Korea a decisive, and completely legitimate, competitive advantage in competing for these types of vessel.

In addition, the cost of materials has fallen and Korean yards have made further productivity gains since 1997. As a result Korean yards have been able to further improve their ability to quote competitive prices.

The depreciation of the Korean Won from around 800 Won to the US Dollar in 1996 to a low of around 1,750 Won to the Dollar in 1997 (yearly average for 1997 1400 Won), gave Korean yards a very substantial further competitive advantage over European yards since shipbuilding contracts are priced in US dollars.

Korean Yards do not enjoy subsidies from the Korean Government, unlike European yards who have enjoyed a range of both open and hidden subsidies over many years. European Yards are unable to compete because of high labour costs, lack of investment, high material costs and failure to achieve productivity levels matching the best Korean and Japanese shipyards. Korean shipyards are not to blame for any of these factors.

In addition, the following factors are important:

1. The availability of competitively priced ships is vital to the World economy which relies on shipping for the vast majority of international trade.

2. Europe's proposals that prices should be increased would adversely impact on renewal of the world tanker fleet, which is necessary to avoid further damage to the environment. Pending IMO rules which have been drafted in the wake of the tanker disasters of recent years provide that single skinned tankers will need to be replaced by double-hulled vessels by 2005. These are also EU initiatives aimed at phasing out single hulls.

3. If the IMO proposals are agreed as expected, around 90 million DWT of new double skinned tankers will need to be built over the next four years. This represents around 30%of the World tanker fleet. It is vital that these tankers are constructed at the most economic price.

4. The Third Party Submissions show that if the price levels at which European and Korean yards bid are similar owners would still choose to build in Korea because of non-price factors including quality, build time and delivery plus after sales service and re-sale value.

5. All of the Third Party Submissions oppose the CESA complaint on substantial grounds. Not one supports the CESA position.

6. Third Party submissions show that owners would not order from European yards even if prices for Korean vessels rose by 20% - 30% as CESA want. Owners would either reduce ordering or would order from Japan at lower price levels or from other yards in countries which may be outside WTO disciplines.

7. Korean yards are a major source of business for European suppliers of marine equipment for the 20% of the materials which are normally sourced outside Korea for vessels built for non-Korean owners. If prices were raised artificially then it is likely that orders would simply transfer to Japan or other countries outside the EU. In the case of Japan almost all of the materials used are domestically sourced and European suppliers of marine equipment would therefore lose out.

8. The Third Pan Submissions point out that even if the price charged by Korean yards to non- Korean owners was artificially raised by 20% - 30% the yards would remain free to sell vessels to domestic Korean shipowners at current economically justified price levels. This would result in European shipowners being at a competitive disadvantage.

For all the reasons set forth in the present paper and based on the economic analysis contained in the Drewry Shipbuilding Report, which should be read together with this Position Paper, the KSA submits that the complaint should be dismissed. Even if the EU wrongly concluded that Korea bestowed actionable subsidies upon its shipbuilding industry(which the KSA strongly denies), the facts prove that such subsidies can not have caused any injury or adverse trade effects. Hence, the prerequisite under the TBR Regulation foi the adoption of commercial measures is absent and no recourse to WTO dispute settlement is warranted.

At the same time. the KSA wishes to emphasise that the EU shipyards have for several decades benefited from openly granted or hidden EU subsidies, which the KSA submits are incompatible with the provisions of the WTO Subsidies Code. The TBR Regulation provides that in the assessment of whether to adopt commercial policy measures, the EU should take into account the broader Community's interests. The KSA believes that it would be against the EU's broader interests to challenge the compatibility of the alleged Korean subsidies for which sound legal arguments confirm the compatibility with the provisions of the WTO Subsidies Code while the EU itself has for years granted subsidies of which a substantial part are even contract-based.

The KSA, therefore, respectfully submits that the TBR examination procedure should be terminated upon a finding of absence of actionable subsidies inflicting injury or adverse trade effects.

ANNEX 1

COMPLETIONS BY YEAR

Year

Korea

Japan

AWES

Otheers

Total

Thou GT

%

Thou GT

%

Thou GT

%

Thou GT

%

Thou GT

%

1948

-

-

-

-

2,116

85.3

366

14.7

2,482

100

1971

-

-

11,132

45.6

10,391

42.6

2,865

11.7

24,388

100

1972

15

0.1

12,857

48.1

10,589

39.6

3,288

12.3

26,749

100

1973

14

0.0

14,751

48.5

11,865

39.0

3,779

12.4

30,409

100

1974

313

0.9

16,894

50.4

12,544

37.4

3,791

11.3

33,542

100

1975

410

1.2

16,991

49.7

13,070

38.2

3,732

10.9

34,203

100

1976

814

2.4

15,868

46.8

12,714

37.5

4,527

13.3

33,923

100

1978

582

2.0

11,708

66.8

10,731

39.0

4,531

16.5

17,532

100

1979

604

3.3

6,307

34.7

6,625

36.4

1,657

25.6

18,196

100

1980

495

3.5

4,697

32.9

4,686

32.8

4,411

30.9

14,289

100

1981

929

5.5

8,400

49.6

4,131

24.4

3,472

20.5

16,932

100

1982

1,401

8.3

8,163

48.5

3,864

23.0

3,392

20.2

16,820

100

1983

1,539

9.7

6,670

41.9

4,224

26.5

3,478

21.9

15,911

100

1984

1,473

8.0

9,711

53.0

3,499

19.1

3,651

19.9

18,334

100

1985

2,620

14.4

9,503

52.3

2,958

16.3

3,076

16.9

18,157

100

1986

3,642

21.6

8,178

48.5

2,059

12.2

2,966

17.6

16,865

100

1987

2,091

17.1

5,708

46.6

1,977

16.1

2,483

20.3

12,259

100

1988

3,174

29.1

4,040

37.0

1,715

15.7

1,980

18.2

10,909

100

1989

3,101

23.4

5,365

40.5

1,988

15.0

2,781

21.0

13,236

100

1990

3,441

23.2

6,663

44.9

2,910

19.6

1,826

12.3

14,840

100

1991

3,737

23.2

7,315

45.4

3,139

19.5

1,931

12.0

16,122

100

1992

4,520

24.5

7,852

42.6

3,268

17.7

2,804

15.2

18,439

100

1993

4,666

23.2

8,930

44.4

4,026

20.0

2,495

12.4

20,117

100

1994

4,230

21.8

8,643

44.6

3,691

19.0

2,820

14.5

19,384

100

1995

6,218

27.8

9,300

41.6

4,244

19.0

2,588

11.6

22,350

100

1996

7,374

28.7

10,182

39.7

4,865

19.0

3,245

12.6

25,666

100

1997

8,124

32.6

9,864

39.6

3,933

15.8

3,005

12.1

24,926

100

1998

7,243

29.0

10,206

40.9

4,424

17.7

3,107

12.4

24,980

100

1999

9,159

33.7

11,070

40.7

3,973

14.6

3,005

11.0

27,207

100

2000 P

11,806

40.6

11,318

38.9

3,514

12.1

2,463

8.5

29,101

100

Source : World Shipbuilding Statistics, Lloyd's Register

Note: 1. Ships over 100 GT

2. From 1996, Poland is included in AWES.

3. P: Preliminary

ANNEX 2

WORLD ORDER BOOK 1 JANUARY 2001

SHIPTYPE

SHIPSIZE

KOREA

JAPAN

EU

CHINA

POLAND

OTHERS

TOTAL SHIPS

TANKER

10〜60K DWT

67

16

20

27

10

30

170

60〜120K DWT

48

16

0

7

0

1

72

120〜200K DWT

45

6

0

0

0

7

58

200K + DWT〜

58

23

0

5

0

0

86

Sub-Total

218

61

20

39

10

38

386

BULK CARRIER

10〜40K DWT

12

43

2

35

0

2

94

40〜60K DWT

10

115

0

21

11

21

178

60〜80K DWT

48

100

0

26

0

2

176

80K + DWT〜

18

44

0

0

0

7

69

Sub-Total

88

302

2

82

11

32

517

CONTAINER

100〜499 TEU

0

0

0

2

0

3

5

Small

500〜999 TEU

0

4

21

9

1

7

42

1,000〜1,999 TEU

11

19

16

17

16

14

93

Medium

2,000〜2,999 TEU

23

4

25

0

32

15

99

3,000〜3,999 TEU

9

0

6

0

10

5

30

Large Post-Panamax

4,000〜8,000 TEU

128

24

1

13

10

3

179

Sub-Total

171

51

69

41

69

47

448

LNG

135-140,000 CBM

11

11

3

0

0

0

25

Sub-Total

488

425

94

162

90

117

1376

Total

513

477

612

293

144

627

2666

Sources:

1. Newbuilding Order book - Simpson Spence & Young

2. LNG - World Shipyard Monitor - Clarksons

3. Total - Lloyd's Register

Note: Norway is classified under EU