The object of this Law is to contribute toward realization of the principles of local autonomy and to strengthen the self-dependence of local bodies, by equalizing the financial resources of local bodies and by assuring the systematic operation of local administration through the establishment of allocation standards of local allocation tax, without impairing the rights of such local bodies to administer their property, perform their affairs and execute their administration autonomously.

(Meaning of Terms)

Article 2.

The following terms as used in this Law shall means as follows:

(1)

"Local allocation tax" shall mean a certain proportion of income tax, corporation tax, liquor tax, consumption tax and tobacco tax respectively computed under Article 6 which is granted by the State to each local body to enable it to perform its functions.

(2)

"Local body" shall mean To, Do, Fu or Ken or City, town or village.

(3)

"Basic financial needs" shall mean the amount computed under Article 11 for the purpose of scientific measurement of the financial needs of a local body.

(4)

"Basic financial revenues" shall mean the amount computed under Article 14 for the purpose scientific measurement of the financial resources of a local body.

(5)

"Yardstick" shall mean a yardstick established for each category of local administration to estimate the scale of local administration according to each category and to serve as the basis of the amount of local allocation tax for each fiscal year.

(6)

"Unit Cost" shall mean the cost for each unit of the yardstick (after modification under paragraph 1 of Article 13, where applicable), based upon the model expenses of a standardized local body for its local administration on a reasonable and appropriate level and for the maintenance of standard facilities, according to Do, Fu or Ken and City, town or village. In computing such unit cost, the expenses to be financed with subsidies, assessments, fees, charges, shares or other related revenues and with the revenues from local tax falling outside of basic financial revenues shall be excluded. The standard sum of expenses for local administration of each category, on the basis of which the ordinary allocation tax is computed, shall be determined by multiplying such unit cost by the numerical value of the yardstick.

(Basic Principles)

Article 3.

The Minister of Public Management, Home Affairs, Posts and Telecommunications shall always endeavor at accurately grasping the financial status of each local body, and, in accordance with this Law, allocate with fairness the total sum of local allocation tax (hereinafter referred to as "allocation tas") to the local bodies whose financial needs exceed their financial revenues, to make good such deficiencies.

(2)

The State shall, in granting allocation tax, respect the principles of local autonomy and shall attach no conditions or impose no limitations on the use thereof.

(3)

Each local body shall make best efforts to maintain a reasonable and appropriate level of administration, and see to it that it conform at least to the minimum standards of scale and quality established by laws or cabinet orders duly delegated by laws.

(Powers and Responsibilities of the Minister of Public Management, Home Affairs, Posts and Telecommunications)

Article 4.

The Minister of Public Management, Home Affairs, Posts and Telecommunications shall have the following powers and responsibilities for the execution of this Law:

(1)

To estimate the total sum of allocation tax to be granted every fiscal year

(2)

To determine the amount of allocation tax to be granted to each local body and grant the same;

(3)

To revise or reduce the amount of allocation tax or order the refundment thereof, under Articles 10, 15, 19 or 20-2;

(4)

To receive appeal for review from a local body under Article 18 and give ruling thereon;

(5)

To receive exception taken by a local body under paragraph 7 of Article 19 (or paragraph 4 of Article 20-2 which adduces the same paragraph of the same article) and give decision thereon;

(6)

To hold a hearing under Article 20;

(7)

To collect and prepare necessary data for estimation of the total sum of allocation tax and computation of the amount of allocation tax to be ranted to each local body;

(8)

To grasp the status of local finance constantly by means of the data collected to improve the operation of allocation tax system;

(9)

To perform the affairs ads provided in this Law, except as enumerated above.

(Data for Computation of Allocation Tax)

Article 5.

The governor of To, Do, Fu or Ken shall, as provided by order of the Ministry of Public Management, Home Affairs, Posts and Telecommunications, present to the Minister of Public Management, Home Affairs, Posts and Telecommunications the data on basic financial needs and basic financial revenues, the data for computation of the amount of special allocation tax and other necessary data related to his To, Do, Fu or Ken, and shall maintain records of basic facts upon which such data are based.

(2)

The Mayor of City, Town or Village shall, as provided by order of the Ministry of Public Management, Home Affairs, Posts and Telecommunications, present to the Governor of To, Do, Fu or Ken the data on basic financial needs and basic financial revenues, the data for computation of the amount of special allocation tax and other necessary data related to his City, Town or Village, and shall maintain records of basic facts upon which such data are based.

(3)

The governor of To, Do, Fu or Ken shall, upon examination, transmit the data submitted under the preceding paragraph to the Minister of Public Management, Home Affairs, Posts and Telecommunications.

(4)

Any administrative organ of the State (which refers to Cabinet Office, Imperial Household Agency, administrative organs under paragraph 1 and 2 of Article 49 of the Cabinet Office Establishment Law (Law No. 89 of 1999) and administrative organs under paragraph 2 of Article 3 of the National Government Organization Law (Law No. 120 of 1948) and shall hereafter be referred to as "administrative organs") concerned with the local administration covered under the basic financial needs shall, upon request of the Minister of Public Management, Home Affairs, Posts and Telecommunications, present to him necessary data for computation and allocation of the allocation tax with respect to the administrative affairs within the power of the organ.

(The Total Sum of Allocation Tax)

Article 6.

The allocation tax shall be equal to 32 per cent of income tax revenue, corporation tax revenue and liquor tax revenue, 29.5 per cent of consumption tax revenue and 25 per cent of tobacco excise revenue.

(2)

The total sum of allocation tax to be granted every fiscal year shall be calculated by summing up 32 per cent each of the estimated revenues of income tax, corporation tax and liquor tax, 29.5 per cent of the estimated revenue of consumption tax, and 25 per cent of the estimated revenue of tobacco excise, plus such portion of the allocation tax for the preceding fiscal years which has yet to be granted, or less such amount granted over and above the due amount in the preceding fiscal years.

(Classification of Allocation Tax)

Article 6-2.

The allocation tax shall be classified into the ordinary allocation tax and the special allocation tax.

(2)

The aggregate sum of the ordinary allocation tax for each fiscal year shall be equal to 94 per cent of the sum referred to in paragraph 2 of the preceding article.

(3)

The aggregate sum of the special allocation tax for each fiscal year shall be equal to 6 per cent of the sum referred to in paragraph 2 of the preceding article.

(Revision of the Amount of the Special Allocation Tax)

Article 6-3.

In case the aggregate sum of the ordinary allocation tax to be granted for a fiscal year exceeds the aggregate sum of the ordinary allocation tax computed for each local body under the first sentence of paragraph 2 of Article 10, such excess shall be added to the aggregate sum of the special allocation tax for the fiscal year.

(2)

In case the aggregate sum of the ordinary allocation tax to be granted continues to show a considerable difference form the aggregate sum of the ordinary allocation tax computed for each local body under the first sentence of paragraph 2 of Article 10 for several consecutive fiscal years, the revision of systems of local finance or local administration, or the change of the rates prescribed in paragraph 1 of Article 6 shall be undertaken.

(Submission and Publication of Estimates of Revenues and Expenditures)

Article 7.

The Cabinet shall every fiscal year prepare a document on the estimates of revenues and expenditures of the whole of the local bodies for the following fiscal year which includes the items below and submit it to the Diet as well as make it public.

(1)

The estimates of the total revenues of the whole of the local bodies and the itemized accounts of the followings:

a.

The standard taxable value, tax rate, estimated amount to be imposed and estimated amount to be collected of each tax items;

b.

Charges and fees;

c.

Debts to be issued;

d.

Disbursements from the State

e.

Other revenues

(2)

Estimates of the total expenditures of the whole of the local bodies and the itemized accounts of the followings:

a.

Itemized total expenditures and the difference from the corresponding amount of the preceding fiscal year;

b.

Total expenditures financed with disbursements from the State

c.

Funds for payment of principal and interest of municipal debts

(Date of Computation)

Article 8.

The amount of allocation tax for each local body shall be computed as of April 1 every fiscal year.

(Abolition, etc. of Local Body)

Article 9.

In case of the abolition, creation, division or merger or the redemarcation of a local body after the date referred to in the preceding paragraph, the following provisions shall be applicable to the allocation tax due to such local body:

(1)

In case the whole area of a local body is annexed to the area of another local body on account of the abolition, creation, division or merger, the sum of the allocation tax due to the local body so annexed shall be granted to the local body to which it is annexed, after the date of abolition creation, division or fusion:

(2)

In case the area of local body is divides on account of the abolition, creation, division or fusion, or is redemarcated, the sum of the allocation tax due to the local body so divided or redemarcated shall, as provided by order of the Minister for Public Management, Home Affairs, Posts and Telecommunications, be divided into portions so that such portions are proportionate to the sums of the allocation taxes which would have been granted to the hypothetical local bodies supposed to have independently existed as of the first April of the same fiscal year over the area affected by such redeemarcation, and such portions shall be granted respectively to the local bodies annexing the area affected by such abolition, creation, division or fusion or redemarcation or the local bodies comprising the area affected by such demarcation.

(Ordinary Allocation Tax)

Article 10.

The ordinary allocation tax shall, as provided by the following paragraph, be granted each fiscal year to such local bodies whose basic financial needs exceed their basic financial revenues.

2.

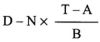

The sum of the ordinary allocation tax to be granted to each local body shall be equal to the excess of its financial needs over its basic financial revenues (hereinafter in this article referred to as "deficiencies"). However, if the total sum of the deficiencies through out all the local bodies exceeds the aggregate sum of the ordinary allocation tax, it shall be equal to the sum calculated by the following formula:

D = Deficiencies of the local body

N = Its basic financial needs

T = Total sum of deficiencies

A = Aggregate sum of the ordinary allocation tax

B = Aggregate sum of the basic financial needs of such local bodies whose basic financial needs exceed its basic financial revenues.

3.

The Minister of Public Management, Home Affairs, Posts and Telecommunications shall be determine the sum of the ordinary allocation tax to be granted under the preceding two paragraphs, not later than the thirty-first of August every year. However, in case of an increase of the aggregate sum of the allocation tax or in other justifiable cases, the sum of the ordinary grant tax may be determined or the already determined sum of the ordinary allocation tax may be revised, on or after the first of September.

4.

The Minister of Public Management, Home Affairs, Posts and Telecommunications shall inform the local body of the sum of the ordinary allocation tax determined or revised under the preceding paragraph.

5.

Even though the already determined sum of the ordinary allocation tax for a local body be revised under the second sentence of paragraph 3, the already determined sums of the local allocation taxes for other local bodies shall not be affected thereby.

6.

If the aggregate sum of the ordinary allocation tax to be granted in a fiscal year falls short of the total sum of the ordinary allocation tax to be granted to each local body as computed under the second sentence of paragraph 2, such deficits shall be covered from the sum of the special allocation tax for the same fiscal year.

(Basic Financial Needs)

Article 11.

The basic financial needs shall be computed by multiplying each unit cost by the numerical value of the applicable yardstick which has been modified under Article 13 and adding together the results thereof.