Japan's Shipbuilding Industry

The Japanese shipbuilding industry has confronted severe recessions twice, in 1979 and 1987, which were caused by the oil crisis and other factors. Various measures including industrial restructuring were taken to overcome the slowdown in business. In 1989, the shipbuilding business showed signs of recovery, resulting from such measures and uptrends in the shipping market. Since then, the Japanese shipbuilding industry has maintained a certain level of shipbuilding operations.

In recent years, however, the foreign exchange rate of the yen has appreciated sharply, and ship prices have fallen. Such factors have made the shipbuilding business more uncertain. In addition, worldwide shipbuilding capacity has increased as seen in growth of the shipbuilding industry of the Republic of Korea (ROK), and the expansion of construction facilities. In the medium term, international competition on shipbuilding is anticipated to become severe after the year 2000, and endeavors are necessary for stable shipbuilding operation.

New orders

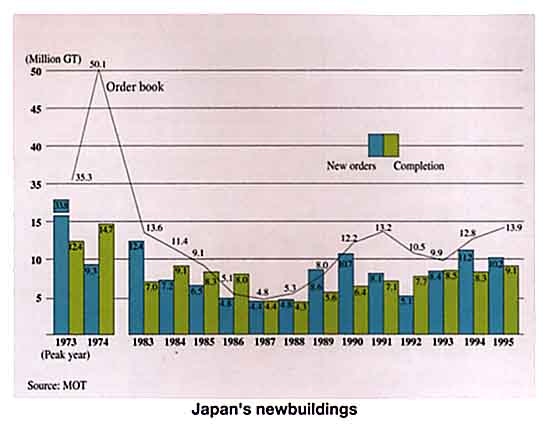

In fiscal 1995, the Japanese shipbuilding industry received newbuilding orders for 393 vessels of 10,224,000GT, a 16% increase in the number of vessels but a 9% decrease in GT, compared with fiscal 1994.

Classified by principal ship types, dry cargo vessels accounted for 8,033,000GT (against 7,592,000 GT in fiscal 1994), tankers for 2,124,000GT (against 3,523,000GT), and others for 67,000GT (against 61,000GT).

Dry cargo vessels, mainly comprising bulk and container carriers as in 1994, accounted for 78% of the total tonnage. Bulk carriers increased by 16% to 6,251,000GT over the preceding year but container carriers decreased by 40% to 1,150,000GT from the preceding year.

Orders for crude oil tankers totaled 1,019,000GT, 10% of the total newbuilding orders, showing a 65% decrease from the preceding year. Newbuilding tankers included four VLCCs of 615,000GT (against 15 of 2,392,000GT in fiscal 1994). Orders for gas carriers in fiscal 1995 included 44 LPG carriers of 397,000GT (against 18 of 244,000 GT in 1994) and 4 LNG carriers of 353,000GT (no orders in 1994).

Classified by domestic and export vessels, ships ordered by domestic owners totaled 684,000 GT (accounting for 7% of the total newbuilding tonnage and up 31% over the preceding year), and export vessels totaled 9,541,000GT (93% of the total tonnage and down 10%).

Worldwide newbuliding orders, according to the Lloyd's Register World Shipbuilding Statistics, increased by 0.7% to 25,529,000 GT in 1995 (calendar year) over the preceding year, of which 8,906,000 GT or 24% less than in 1994 was ordered from Japanese shipyards (representing a share of 34.9%), 4,310,000GT or 29% more than the preceding year, from West European shipyards (16.9%), and 7,762,000GT or 37% more, from ROK shipyards (30.4%). For reference, newbuilding orders world-wide for the first quarter of 1996 accounted for 5,441,000GT, of which 2,237,000GT (41%) was ordered from Japanese shipyards, 868,000GT (16%), from West European shipyards, and 1,176,000GT (22%), from ROK shipyards.